Future Developments - Constraints

Global Common Document Taxonomy (INT-GCD)

Accountant’s Report Taxonomy (INT-AR)

IFRS-CI – Taxonomy (this Taxonomy)

1.5. Relationship to Other Work

2. Overview of the IFRS-CI Taxonomy

Future Developments - Different Presentations

2.3. Element Naming Convention

Future Developments – Structured References

2.6. Additional Documentation Available

3. Points to Note in Using the IFRS-CI Taxonomy

3.2. How to Interpret the Taxonomy Structure

3.4. Income Statement Structure

3.5. Statement of Cash Flows Structure

3.6. Statement of Changes in Equity Structure

Assets and Liability and Equity Disclosures

3.9. Type Enumeration Elements

3.10. Equivalent facts (same-as, essence-alias)

3.15. Entering Numeric Values into Instance Documents

Sample Company Sample Instance Document

5.3. Errors and Clarifications

9. Intellectual Property Status

1. Overview

1.1. Purpose

The International Accounting Standards Committee Foundation (IASC Foundation, http://www.iascf.com) and the IFRS Taxonomy Working Group of XBRL International (http://www.xbrl.org) have developed a comprehensive eXtensible Business Reporting Language (XBRL) Taxonomy that models the financial statements that a commercial and industrial entity may use to report under International Financial Reporting Standards (IFRS) (http://www.iasb.org.uk).

The International Financial Reporting Standards (IFRS), Financial Reporting for Commercial and Industrial Entities (CI) Taxonomy (the IFRS-CI Taxonomy) includes XBRL representations of the primary financial statements (balance sheet, income statement, statement of changes in equity and cash flow statement), together with accounting policies and explanatory disclosures.

Note that previous published versions of this Taxonomy consisted of separate XBRL schema containing the Primary Financial Statement elements (PFS Taxonomy) and the Explanatory Disclosures and Accounting Policies elements (EDAP Taxonomy). This release of the Taxonomy consolidates the PFS and EDAP taxonomies into a single Taxonomy, the IFRS-CI Taxonomy.

The IFRS-CI Taxonomy defines the XBRL standard for IFRS-CI elements, but in no way defines IFRS, how financial statements are presented or what must be disclosed in the financial statements.

The primary goal of the IFRS Taxonomy Working Group, in developing the IFRS-CI Taxonomy, is to build a Taxonomy that captures the elements most commonly observed in financial statements used in practice. The total set of elements included in the IFRS-CI is larger than the set of elements IFRS requires to be disclosed in the financial statements. The additional elements are included because they are either commonly observed disclosures under IFRS or are required to ensure structural integrity of the financial statements. For example, nothing in IFRS requires the disclosure of “Total Liabilities and Equity”, yet it is a common element observed in financial statements prepared under IFRS.

The purpose of this and other taxonomies produced using XBRL is to facilitate data exchange among applications used by companies and individuals as well as other financial information stakeholders, such as lenders, investors, auditors, attorneys, and regulators.

The IFRS-CI Taxonomy design will facilitate the creation of XBRL instance documents that capture business and financial reporting information for commercial and industrial entities according to the International Accounting Standards Board’s (http://www.iasb.org.uk) International Financial Reporting Standards (incorporating International Accounting Standards and Interpretations). The IFRS-CI Taxonomy provides a framework for consistent identification of elements when entities create XBRL documents under that Taxonomy. Typically, documents prepared in relation to this Taxonomy can facilitate the reporting requirements of corporations to make annual, semi-annual or quarterly disclosures to stakeholders and capital markets.

1.2. Authority

The authority for this IFRS-CI Taxonomy is based upon the International Accounting Standards Board’s (http://www.iasb.org.uk) International Financial Reporting Standards incorporating International Accounting Standards (IAS) and interpretations issued by the SIC effective 01 January 2003 (http://www.iasc.org.uk/cmt/0001.asp?s=100064351&sc ={311C5B23-730E-11D5-BE5E-003048110251}&n=63). The IFRS-CI Taxonomy also includes non-authoritative “common practices,” where the Standards and interpretations are silent on common patterns of financial reporting.

As this Taxonomy primarily addresses the reporting considerations of commercial and industrial entities, IAS 26 (Accounting and Reporting by Retirement Benefit Plans) and IAS 30 (Disclosures in the Financial Statements of Banks and Similar Financial Institutions) disclosure requirements are not represented in the IFRS-CI Taxonomy’s content.

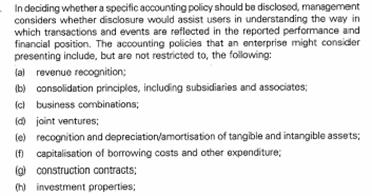

The particular disclosures this IFRS-CI Taxonomy models are those:

1. Required by particular IFRSs

2. Typically represented in IFRS model financial statements, checklists and guidance materials as provided from each of the major international accounting firms.

3. Found in common practice financial reporting, and

4. Flow logically from items 1-3, for example, sub-totals and totals.

This IFRS-CI Taxonomy is in compliance with XBRL Specification Version 2.0a, dated 2001-11-15 [XBRL].

1.3. Taxonomy Status

The IFRS-CI Taxonomy is an Acknowledged Public Working Draft. Its content and structure have been reviewed by both accounting and technical teams of the IASC Foundation (http://www.iascf.com) and the IFRS Taxonomy and XBRL Specification Working Groups of XBRL International.

XBRL Taxonomies can exist in five states insofar as XBRL International is concerned:

- Working Draft – Draft of an International Working Group.

- Unacknowledged - Developed externally but not royalty-free, or not known to be spec compliant.

- Acknowledged - Developed externally, compliant with the specification, and minimally 'advertised' by XBRL International.

- Approved - Acknowledged, and also complying with published best practices.

- Recommended - Approved, and recommended because it is better than alternative taxonomies for the same purpose.

The following is a summary of levels of approval attainable within each state of Taxonomy approval outlined above:

- Internal Working Draft – Internal Working Draft version of a Taxonomy exposed to XBRL International members for internal review and testing. An Internal Working Draft is subject to significant changes as initial testing undertaken. Its structure may not be stable and its content may not be complete.

- Public Working Draft – Working Draft version of a Taxonomy exposed to public for review and testing. A Public Working Draft has been tested and its structure is unlikely to change although its contents may still change as the result of broader testing.

- Final – Final version of a Taxonomy, designated by XBRL International as the most appropriate representation of a particular reporting environment.

Future Developments - Constraints

The development of this Taxonomy placed large resource demands on the members of the IFRS Taxonomy Working Group. XBRL itself is evolving rapidly and, in many instances, the Group had no precedents to follow. Further, all participants in the Group are volunteers and there have been many occasions when competing demands have impacted the amount of time people have been able to devote to the project.

These factors demanded that the Working Group limit the scope of the IFRS-CI Development to ensure a complete commercial and industrial Taxonomy version was delivered. This is a first, but significant, step in IFRS Taxonomy development. The Group learned a lot completing the project. Not everything that was learned has been incorporated in this version of the Taxonomy, it will be incorporated in future releases - in particular, the impending release under XBRL 2.1 specification when that specification is finalised.

1.4. Scope of Taxonomy

This Taxonomy is the IFRS-CI Taxonomy. The IFRS-CI Taxonomy is intended to be used with the XBRL Global Common Document (INT-GCD) Taxonomy, and the Accountant’s Report (INT-AR) Taxonomy. In addition, other national jurisdictions and industries may leverage the IFRS-CI, INT-GCD, and INT-AR. This section describes the relationship between these taxonomies.

Global Common Document Taxonomy (INT-GCD)

The INT-GCD Taxonomy incorporates elements that are common to the vast majority of XBRL instance documents. The INT-GCD Taxonomy has elements that describe the XBRL instance document itself and the entity to which the instance document relates. The Taxonomy was co-developed by the IFRS Taxonomy Development and XBRL US Domain Working Groups. See http://www.xbrl.org for the latest version of the INT-GCD Taxonomy.

Accountant’s Report Taxonomy (INT-AR)

The INT-AR Taxonomy is intended to provide information related to the auditor’s/independent Accountants Report that typically accompanies external financial reports of public companies. The Taxonomy was developed by the XBRL International Accounting Supply Chain Working Group with input from IFRS Taxonomy Development and XBRL US Domain Working Groups. See http://www.xbrl.org for the latest version of the INT-AR Taxonomy.

IFRS-CI – Taxonomy (this Taxonomy)

The IFRS-CI Taxonomy encompasses the financial statements that private sector and certain public sector entities typically report in annual, semi-annual or quarterly financial disclosures as required by IAS 1, paragraph 7 (revised 1993) and IAS 34, paragraph 8 (revised 1998).

Those financial statements are the:

- Balance Sheet

- Income statement

- Statement of Cash Flows

- Statement of Changes in Equity

- Accounting Policies

- Explanatory Disclosures

and their condensed equivalents.

Reporting elements from those financial statements may be incorporated into a wide variety of other disclosures from press releases to multi-period summaries.

IFRS Framework

Used together, these taxonomies will meet the reporting needs of entities that meet three criteria, viz (i) report under International Financial Reporting Standards (incorporating International Accounting Standards and interpretations), (ii) are in the broad category of “commercial and industrial” industries and (iii) have relatively common and consistent set of reporting elements in their financial statements. Whilst many reporting entities meet these three criteria, there are entities require different or additional elements (i.e. extension taxonomies) to those captured in this Taxonomy.

For this reason, additional taxonomies that represent extensions to IFRS-CI are likely to be required. These taxonomies are likely to identify the particular needs of:

- International industries, for example, airlines, pharmaceuticals or agribusiness.

- National jurisdictions. The accounting standards in many countries are substantially based on IFRS. However, timing differences in adoption or additional requirements may exist.

- National industry or common practice, for example, agriculture or credit reporting.

- Individual entities and their specific reporting requirements. These extension taxonomies will either extend the INT-GCD, INT-AR, and IFRS-CI taxonomies to meet the particular reporting requirements of that industry, country or entity and/or restrict the use of particular taxonomies by limiting the use of particular IFRS-CI Taxonomy elements.

The inter-relationships of the various taxonomies are show in Figure 1:

Figure 1: Interrelationship of Taxonomies and Instance Document

At the date of release of this document some of these taxonomies have been created and released and others have not been created or have not been released. However, extension taxonomies are under development for some national jurisdictions and within certain industries.

1.5. Relationship to Other Work

XBRL utilises the World Wide Web consortium (W3C http://www.w3.org ) recommendations, specifically:

- XML 1.0 (http://www.w3.org/TR/2000/REC-xml-15001006)

- XML Namespaces (http://www.w3.org/TR/1999/REC-xml-names-19990114/)

- XML Schema 1.0 (http://www.w3.org/TR/xmlschema-1/ and http://www.w3.org/TR/xmlschema-2/), and

- XLink 1.0 (http://www.w3.org/TR/xlink/).

2. Overview of the IFRS-CI Taxonomy

The following is an overview of the Taxonomy. It is assumed that the reader is familiar with financial and business reporting and has a basic understanding of XBRL.

2.1. Contents of the Taxonomy

This IFRS-CI Taxonomy makes available to users the most commonly disclosed financial information under International Financial Reporting Standards (incorporating International Accounting Standards and interpretations). This Taxonomy is an expression of financial information in terms that are understandable to humans, but equally as important understandable by a computer applications.

The IFRS-CI Taxonomy is made up of a “package” of interrelated XML files:

- XML Schema File (.XSD files): An XBRL Version 2.0 Taxonomy XML Schema file.

- XBRL Linkbases (.XML files): “Linkbases” for:

- Labels

- References

- Presentation relationships between elements;

- Calculation relationships between elements; and

- Definitional relationships between elements.

The package is represented visually, with an example based on Balance Sheet reporting of Non Current Investment Property is shown in Figure 2:

Figure 2: IFRS-CI Taxonomy Package with Descriptions and Examples

The diagram above shows that a Taxonomy is a collection of one or more XML Schema files. The XML Schema is further described by a number of linkbases.

Two XML Schema files are provided with this Taxonomy. The first XML Schema file (http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15.xsd) contains Taxonomy elements and links ONLY to the references linkbase. The second XML Schema file (http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-WINDOW.xsd) imports the first XML Schema file and provides links to ALL linkbases.

The purpose of providing these two files (a schema file and a schema “Window Taxonomy”) is to enable users of the Taxonomy the flexibility of selecting the linkbases they wish to make use of, rather than forcing the use of all linkbases under a single schema file. For example, accounting jurisdictions may not wish to use English labels. Similarly, they may wish to redefine element calculation, definition or presentation links.

2.2. Taxonomy Structure

Overview

The IFRS-CI Taxonomy contains approximately 3240 XBRL elements, which are unique, individually identified pieces of information. The XML schema file is the foundation of the Taxonomy package and provides a straightforward listing of the elements in the Taxonomy. The associated linkbases provide the information that is necessary to interpret (e.g. Label and Definition linkbases) Taxonomy elements or place a given Taxonomy element in context of other Taxonomy elements (e.g. Calculation and Presentation linkbases).

Viewing a Taxonomy

The actual IFRS-CI Taxonomy comprises an XSD file and five linkbases that express Taxonomy element relationships. Viewing the full relationship between the XML Schema and the linkbase files requires a Taxonomy Builder. For review purposes a paper based representation, in Adobe Acrobat (PDF) or Excel, is the most practical solution. The disadvantage is that, in this printed form, many of the characteristics of taxonomies are not obvious. Printed versions are two-dimensional, whereas the information in the Taxonomy is multi-dimensional.

Element Organisation

Users of the Taxonomy need to be able to locate Taxonomy elements, so that they can be mapped to the information systems from which data is drawn to generate XBRL Instance Documents. There are many ways the elements could have been organised, including, for example, alphabetical order. The IFRS-CI Taxonomy is organised using a “Balance Sheet” metaphor. That is, the elements are organised using the most commonly observed financial statement presentation style based on the organisation of elements in the balance sheet. This type of organisation was adopted because it is used by many financial statement stakeholders. For example audit working papers are often prepared using this structure. Users are also clearly familiar with how financial statements are generally organised.

However, this metaphor and organisation may limit the understanding of the underlying complexity and ultimate power of an XBRL Taxonomy. A Taxonomy has multiple “dimensions”. Relationships can be expressed in terms of definitions, calculations, links to labels in one or more languages, links to one or more references, etc. The metaphor used expresses only one such set of relationships, which is presentation-based and in English. There is also a danger that users will perceive that the way the elements are organised implies that this is how financial statements should be rendered. This is simply not the case. The way the Taxonomy is organised is to help users find elements, not to prescribe a presentation format.

The IFRS-CI Taxonomy is divided logically into sections that correspond to typical financial statement components. For example, the Balance Sheet section or the Income Statement section. While there is no true concept of “sections” or groupings in the Taxonomy, their purpose is simply to group similar concepts together and facilitate navigation within the Taxonomy.

Within these sections the IFRS Taxonomy Working Group needed to choose between alternative ways of grouping elements. For example, IFRSs do not define “Finance Costs,” yet IAS-1 requires the disclosure of this item on the face of the Income Statement. Model financial statements produced by the major international accounting firms define this component differently. Some present a net finance cost figure while others treat is as a gross expense. The IFRS-CI Taxonomy presents it as a gross expense, but this does not prohibit a user from netting the revenue and expense components. Again, the IFRS-CI does not define IFRS. The organisation of the Taxonomy is designed to help users locate elements.

Abstract XML elements, for example “Balance Sheet (Classified)” (ID 7) and “Income Statement” (ID 202) provide the ability to express “groupings” of elements within an XBRL Taxonomy. Abstract XML elements can never hold values. They are purely structural in nature and are used to create artificial “sections” or “groupings” in a Taxonomy.

The following is a listing of the higher-level “sections” within the IFRS-CI Taxonomy which are discussed in this document:

Figure 3: High Level Sections of IFRS-CI Taxonomy

|

Section |

Explanatory Guidance |

|

Balance Sheet (Classified) |

See Section 3.3 |

|

Income Statement |

See Section 3.4 |

|

Statement of Cash Flows |

See Section 3.5 |

|

Statement of Changes in Equity |

See Section 3.6 |

|

Accounting Policies |

See Section 3.7 |

|

Explanatory Disclosures |

See Section 3.8 |

|

Type Enumeration Elements |

See Section 3.9 |

Future Developments - Different Presentations

Taxonomies can be viewed in different ways, using multiple “filters” or presentation linkbases with each meeting the particular needs of a user group. For example, filters may be generated that allow a user to view the elements in a Taxonomy that relate to a particular financial statement section or note, or a specific accounting standard.

Placement of financial information elements into different parts of a Taxonomy (i.e. primary financial statements or notes) is inherently arbitrary and may create conflicts for different user groups. It is likely that the multiple filter solution, with multiple views of the same data, will dominate to solve this issue. Whatever the direction, it is clear that the management of Taxonomies will need to evolve to meet this user demand.

2.3. Element Naming Convention

The convention for naming XBRL elements within a Taxonomy follows that of XML Schema. Each name within a Taxonomy must be unique and must start with an alpha character or the underscore character. Element names are case-sensitive. The IFRS-CI Taxonomy naming convention follows these rules; see the XML Specification for more information (refer to Section 1.5 above).

In addition to following XML Schema naming requirements, the IFRS-CI Taxonomy places additional constraints on element naming based on an element naming convention developed by the IFRS Taxonomy Working Group and the US Taxonomy Working Group. Companies creating extension taxonomies are encouraged to follow this XBRL “best practices” naming convention, but are not required to do so.

The naming convention used encourages camel case names (e.g. the term “Balance Sheet” becomes BalanceSheet) which use descriptive names for readability and are common in other XML languages.

Certain short connector words are dropped when labels are converted to element names including, but not limited to:

an, and, any, are, as, at, be, but, by, can, could, does, for, from, has, have, if, in, is, its, made, may, of, on, or, such, than, that, the, this, to, when, where, which, with, would.

2.4. Label and Languages

In this release, labels for Taxonomy elements are provided in English. Additional linkbases will be subsequently developed to express Taxonomy labels in other languages, for example French or Japanese. These labels will be represented in separate label linkbases.

The labels provided in the IFRS-CI Taxonomy are not intended to be the exact labels used in financial reporting. The labels are often more verbose descriptors to help the user understand the Taxonomy element.

The IFRS-CI Taxonomy relies on IFRS to define the meaning of each element. No definitions are provided within the Taxonomy.

Each label in the Taxonomy is unique within this Taxonomy in order to make using the Taxonomy easier and to assist a user to understand what an element might represent. These “verbose” labels may be supplemented by other labels which have the more precise term commonly used in financial statements.

2.5. References

This IFRS-CI Taxonomy provides references to IFRS standards and other authoritative sources. Reference information is captured in the Taxonomy reference linkbase using the following element names: Name, Number, Paragraph, Subparagraph, and Clause.

Sources for references provided in the IFRS-CI Taxonomy include:

- IFRS standards, referenced as: IFRS x para y(z) or IAS x para y(z)

- IFRIC and SIC interpretations referenced as: IFRIC x para y(z) or SIC x para y(z)

- IFRS common practice, referenced as: IFRS-CP

- Structural completeness (i.e. a sub-total), referenced as: IFRS-SC

- XBRL related (i.e. a type), referenced as: XBRL

For this version of the IFRS-CI Taxonomy, minimal referencing is provided.

Future Developments – Structured References

The editors of this Taxonomy acknowledge that enhanced referencing schemes provide better information with respect to Taxonomy elements. Feedback has been received that the inclusion of an IFRS reference for a particular element in the IFRS-CI Taxonomy implies that that element must be disclosed on the face of the primary financial statements. In many cases the detailed elements included in the IFRS-CI Taxonomy are commonly observed in practice, but not necessarily required to be disclosed on the face. Typically, IFRS will require a summary component, such as total property, plant and equipment, be disclosed. The IFRS-CI Taxonomy captures this requirement, but also provides a list of sub-elements of classes of property, plant and equipment because this is common practice.

A revised reference scheme is likely to be incorporated in the construction of future versions of this Taxonomy, or provided by third parties, that ensures that the referencing system distinguishes between the absolute minimum disclosures specified under IFRS and the commonly observed disclosures. The referencing system is also likely to indicate the IFRS reference that defines an item and, in the case of common practice, what influenced the inclusion of an element in the Taxonomy.

2.6. Additional Documentation Available

The intention of this document is to explain the IFRS-CI Taxonomy. This document assumes a general understanding of accounting and XBRL. If the reader desires additional information relating to XBRL, the XBRL International web site (http://www.xbrl.org) is recommended. Specifically, a reading of the XBRL Specification Version 2.0a [XBRL] is also encouraged. The purpose of this document is to explain how XBRL is applied in this specific case of the IFRS-CI Taxonomy.

The following documentation is available to assist those wishing to understand and use this Taxonomy. This documentation is available on the XBRL International web site (http://www.xbrl.org):

Explanatory Notes (this document)

This is an overview document describing objectives of the IASC Foundation, XBRL International IFRS Working Group and the IFRS-CI Taxonomy:

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15.htm (HTML Format)

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15.pdf (PDF Format)

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15.doc (Word Format)

Taxonomy Elements

This is a summary listing of Taxonomy elements in a human readable format for the purpose of obtaining an overview of this Taxonomy.

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-elements.pdf (PDF Format)

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-elments2.pdf (PDF Format, element labels and element names)

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-elements.xls (Excel Format)

Taxonomy Package

The following ZIP file contains the Taxonomy package, Taxonomy documentation, and sample instance documents: http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15.zip

These files are located as follows:

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15.xsd (Schema linked only to references linkbase)

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-WINDOW.xsd (Schema linked to all linkbases, “Window Taxonomy”)

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-references.xml (References linkbase)

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-labels.xml (Labels linkbase)

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-presentation.xml (Presentation linkbase)

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-calculation.xml (Calculation linkbase)

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-definition.xml (Definition linkbase)

“Sample Company” Instance Documents (Non Normative)

The “Sample Company” instance documents are provided as a practical example of the application of the Taxonomy. The instance document is provided in un-styled XML; and in Adobe Acrobat:

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/SampleCompany-2003-07-15.xml (XBRL/XML Format)

http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/SampleCompany-2003-07-15.pdf (PDF Format)

3. Points to Note in Using the IFRS-CI Taxonomy

3.1. Introduction

The following explanation of the IFRS-CI Taxonomy, the taxonomies with which this IFRS-CI Taxonomy is designed to interoperate, and examples of how to interpret the IFRS-CI Taxonomy are provided to make the IFRS-CI Taxonomy easier to use. Please refer to the detailed printout of the IFRS-CI Taxonomy element ID numbers as you read this explanation (http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-elements.pdf).

An alternative printout which contains labels and element names is available at (http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15-elements2.pdf).

This explanatory document is designed to provide an overview of the IFRS-CI Taxonomy. It is anticipated that the XBRL community will create courses, books and other materials to provide a thorough explanation of every aspect of using the IFRS-CI Taxonomy and other XBRL taxonomies.

Please note that element names are provided ONLY in the first example below (Figure 4: Sample Elements) in order to show the difference between element names and element labels. Element labels are not shown in subsequent examples. Elements can be referenced to the taxonomy printouts using the “ID” provided in this documentation, and is shown in the taxonomy printouts. Note that the ID is for informational purposes and ease of cross-referencing information ONLY and is not part of XBRL. Also note that each element label in the IFRS-CI taxonomy is unique.

3.2. How to Interpret the Taxonomy Structure

The IFRS-CI Taxonomy does not present anything new to accountants or analysts who understand financial information. However, the way the information is structured in the printed version is most likely very new to participants in the financial reporting supply chain. This section of the IFRS-CI Taxonomy documentation provides an explanation of the IFRS-CI Taxonomy in both narrative and graphical forms. This explanation is non-normative and the XML schema file and linkbases that explain the Taxonomy in terms a computer can interpret takes precedence over this explanation.

The element fragments shown in Figure 4 exists within the “Non Current Assets” section contained within the “Assets” section of the “Balance Sheet – (Classified)” section of the IFRS-CI Taxonomy:

Figure 4: Sample Elements

|

Element Label |

Element Name |

ID |

|

Non Current Assets |

NonCurrentAssets |

9 |

|

Property, Plant and Equipment |

PropertyPlantEquipment |

10 |

|

Investment Property |

InvestmentProperty |

11 |

|

Intangible Assets |

IntangibleAssets |

12 |

This means that for a commercial and industrial entity, there is a type of non-current asset called “Property Plant and Equipment”. This concept is represented in the IFRS-CI Taxonomy by an element with the name “PropertyPlantEquipment” and the English label “Property, Plant and Equipment”.

When an entity reports “Property, Plant and Equipment” as a component of its financial results in an XBRL instance document, it will typically report this element as the sum of specific sub-elements of property, plant and equipment (e.g. Construction in Progress, Land, Buildings, Plant and Equipment, etc.). The element “Property, Plant and Equipment” will, then, have subsidiary elements (children) that sum (“roll up”) to the total of “Property, Plant and Equipment”. In an XBRL instance document one of the following will be true:

· The total amount of “Property, Plant and Equipment” will be included in the single element “Property, Plant and Equipment.”

· The values of “Property, Plant and Equipment” of the entity will be recorded within one or more of the child elements provided in the IFRS-CI Taxonomy.

· The preparer of the instance document will create an extension Taxonomy and create new children within “Property, Plant and Equipment.” The values of “Property, Plant and Equipment” of the entity would be recorded win one or more of the existing children to “Property, Plant and Equipment” in the IFRS-CI Taxonomy, or to one or more of the extension Taxonomy elements.

All of the elements in the fragment shown are of the XBRL data type “monetary” and have a weight equal to “1”. Having a weight equal to “1” indicates that in an instance document, the value of all children of an element, when multiplied by the assigned weight, adds (or “rolls”) up to the value of the parent element. For example, “Property Plant and Equipment,” “Investment Property” and “Intangible Assets” are components of the total value of “Non Current Assets,” as are other assets such as “Biological Assets” (ID 13) and “Investments in Subsidiaries, at Cost (ID 16). The mathematical relationship between these elements is represented in the Calculation linkbase. In this linkbase, “Assets” has a value equal to the value of its two children “Current Assets” (ID 27) and “Non Current Assets”. These numeric relationships are found throughout the Taxonomy. These relationships are represented in the calculation linkbase.

The Taxonomy is structured so that parent elements precede their child elements. For example, a child of the Income Statement element, “Net Profit (Loss) Transferred to Equity” (ID 203) precedes the other elements in the Income Statement such as “Extraordinary Items of Income (Expense), After Tax”, (ID 261) or “Net Profit (Loss) from Ordinary Activities” (ID 204). This pattern is followed throughout the Taxonomy.

3.3. Balance Sheet Structure

Three balance sheet formats are provided with the IFRS-CI Taxonomy:

· Classified

· Order of Liquidity

· Net Assets Format

The classified balance sheet will be used to explain the major sections of the balance sheet and how they relate to one another.

The major sections of the Balance Sheet structure are shown in Figure 5:

Figure 5: Balance Sheet Major Structures

|

Element Labels |

ID |

|

Balance Sheet (Classified) |

7 |

|

Assets (Classified) |

8 |

|

Non Current Assets |

9 |

|

Current Assets |

27 |

|

Liabilities and Equity (Classified) |

38 |

|

Equity Plus Minority Interest |

39 |

|

Equity, Parent |

40 |

|

Minority Interests in Net Assets |

47 |

|

Liabilities |

48 |

|

Non Current Liabilities |

49 |

|

Current Liabilities |

59 |

The balance sheet structure is intuitive. The Balance Sheet has Assets, Liabilities, and Equity sections. Both Assets and Liabilities have Non Current and Current sections, corresponding to a classified Balance Sheet.

Figure 6: Balance Sheet Fragment

Figure 6 shows a fragment of the Balance Sheet, Non Current Assets. The elements “Property, Plant and Equipment”, “Investment Property”, and “Intangible Assets” are Non Current Assets. “Property, Plant and Equipment” also has children including “Construction in Progress”, etc.

3.4. Income Statement Structure

The structure of the Income Statement and Cash Flows statement (see Section 3.5), and other structures, may appear counter-intuitive initially. The major sections of the Income Statement are shown in Figure 7:

Figure 7: Income Statement Major Structures

|

Element Labels |

ID |

|

Income Statement |

202 |

|

Net Profit (Loss) Transferred to Equity |

203 |

|

Earnings Per Share |

265 |

The Income Statement has two major sections. “Net Profit (Loss) Transferred to Equity” and “Earnings Per Share” information.

The structure of one “tree” section of the Income Statement, which will help explain the structure of the Income Statement is shown in Figure 8:

Figure 8: Income Statement Fragment

An Income Statement's fundamental purpose is to derive Net Income for an entity, and the items which comprise that Net Income. The final result is “Net Profit (Loss) Transferred to Equity” - commonly referred to as “Net Income”.

One section of the structure from Figure 8, “Profit (Loss) After Tax” is explained as follows. This element is comprised of other elements:

· Income Tax Expense (Income)

· Profit (Loss) Before Tax

The element “Profit (Loss) Before Tax” has more detailed children: “Gains (Loss) on Disposal of Discontinuing Operations”, “Gains (Loss) on Remeasurement of Available for Sale Financial Assets”, “Gain (Loss) on Financial Instruments Designated as Cash Flow Hedges”, etc. The last of these items, “Profit (Loss) from Operations” further breaks down into “Profit (Loss) from Operations [by function]” and “Profit (Loss) from Operations [by nature]”.

Important note: Generally entities break down “Profit (Loss) from Operations” by nature, or by function, not both. Both options for breaking down “Profit (Loss) from Operations” are provided, however, only one should be used.

Important note: There is a “same-as” relationship between both “Profit (Loss) from Operations [by function or by nature]” and “Profit (Loss) from Operations [by nature]” and “Profit (Loss) from Operations [by function]”. See section 3.7 relating to “Equivalent Facts” for further discussion.

3.5. Statement of Cash Flows Structure

The major sections of the Income Statement are shown in Figure 9:

Figure 9: Statement of Cash Flows Major Structures

|

Element Labels |

ID |

|

Statement of Cash Flows |

272 |

|

Cash and Cash Equivalents, Ending Balance |

273 |

|

Cash and Cash Equivalents, Beginning Balance |

274 |

|

Effect of Exchange Rate Changes on Cash and Cash Equivalents |

275 |

|

Net Increase (Decrease) in Cash and Cash Equivalents |

276 |

|

Net Cash Flows from (Used in) Operating Activities |

277 |

|

Net Cash Flows from (Used in) Investing Activities |

362 |

|

Net Cash Flows from (Used in) Financing Activities |

405 |

The structure of the Cash Flows disclosures is shown in Figure 10:

Figure 10: Statement of Cash Flows Fragment

Fundamentally, the Cash Flows statement provides a reconciliation between Beginning and Ending Cash and breaks the net change into cash flows provided by Operating Activities, Investing Activities, and Financing Activities. Each of these major sections is further broken out into more detailed sections.

Important Note: The structure of the Cash Flows disclosures is closely modelled on the disclosures required in IAS 7. Support is provided for both the direct and indirect methods. However, only one of these methods is used in a cash flows statement. There is a “same-as” relationship between both “Net Cash Flows from (Used in) Operating Activities [Direct or Indirect Method]” and “Cash Flows from (Used in) Operations [Indirect Method]” and “Cash Flows from (Used in) Operations [Direct Metnod]”. See section 3.7 relating to “Equivalent Facts” for further discussion.

Important Note: It would be very rare for the creator of an XBRL instance document to use the beginning balance element “Cash and Cash Equivalents, Beginning Balance.”

3.6. Statement of Changes in Equity Structure

Figure 11: Statement of Changes in Equity Major Structures

|

Element Labels |

ID |

|

Statement of Changes in Equity |

427 |

|

Issued Capital Movements |

428 |

|

Reserves Movements |

498 |

|

Treasury Shares Movements |

650 |

|

Retained Profits (Accumulated Losses) Movements |

664 |

|

Equity, Total, Ending Balance |

688 |

For each of the sections of the Statement of Changes in Equity, there are components that contain the details of that section. For example, the details of “Issued Capital Movements” include: “Share Capital, Ordinary Shares”, “Share Premium, Ordinary Shares”, “Share Capital, Preference Shares”, and “Share Premium, Preference Shares”. Each of these sections has a reconciliation between the beginning balance and ending balance of that equity account, and shows the changes in that equity account. In addition, adjustments to the beginning balance of equity are provided.

The structure of one of these detail sections is illustrated by the elements for disclosures in changes in Share Capital, Ordinary Shares, as shown in Figure 12:

Figure 12: Statement of Changes in Equity Fragment

Important Note: The section “Equity, Total, Ending Balance” is equivalent to the totals column of a statement of changes in equity. This section ties to the “Equity” element of the balance sheet.

Important Note: It would be very rare for a creator of an XBRL instance document to use the beginning balance elements, for example “Share Capital, Ordinary Shares, Beginning Balance”.

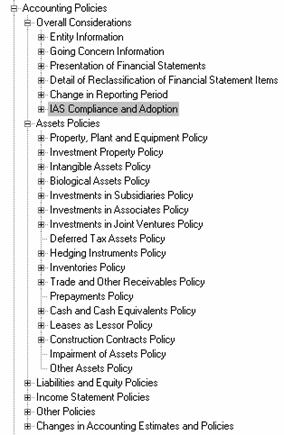

3.7. Accounting Policies

The Accounting Policies section of the IFRS-CI Taxonomy is designed to provide pointers to appropriate constituents of accounting policies adopted by entity. This disclosure is typically made in the first note to the financial statements. A sample of elements of the Accounting Policies section of the IFRS-CI Taxonomy is shown in Figure 13:

Figure 13: Structure of Accounting Policies

Within each of these major sections are a variety of elements that meet the particular reporting requirements of corporations and the IFRS standards. For example, the element labeled “Investment Property Policy” is the element that represent entity’s accounting policies of its accounting for Investment Properties. This IFRS-CI taxonomy element is derived from the disclosures suggested in IAS 1 Para 99, as shown in the following figure:

Figure 14: Accounting Policies - Investment Properties

There are ten other elements that relate to this element, most of which derive their authority from IAS 40, as shown in Figure 15:

Figure 15: Investment Property Disclosures

|

ID |

Label |

Authority |

|

862 |

Investment Property Policy |

IAS 1 99 h |

|

863 |

Model Used to Measure Investment Property (Cost or Fair Value) |

IAS 40 24 |

|

864 |

Cost Model Policies |

IAS 40 50 |

|

865 |

Estimated Useful Lives or Depreciation Rates |

IAS 40 69 b |

|

866 |

Method Used for Depreciating Investment Property(Life or Rate) |

IAS 40 69 a |

|

867 |

Life or Rate for Investment Property |

IAS 40 69 b |

|

868 |

Minimum Life or Rate for Investment Property |

IAS 40 69 b |

|

869 |

Maximum Life or Rate for Investment Property |

IAS 40 69 b |

|

870 |

Subsequent Measurement Using Cost Model |

IAS 40 1 99 h |

|

871 |

Fair Value Model Policies |

IAS 40 27 |

|

872 |

Basis Used to Determine Fair Value |

IAS 40 66 b |

This basic pattern continues for all accounting policies. A total of approximately

300 elements in the IFRS-CI Taxonomy are for the accounting policies of the entity.

Particular entities will make the judgment as to whether they will disclose

their accounting policies at a higher level, for example at the level of the

element labeled “Investment Property Policy” or at a more detailed level, for

example at the level of the element labeled “Maximum Life or Rate for Investment

Property”.

3.8. Explanatory Disclosures

The elements that relate to the financial disclosures found in Balance Sheet, Income Statement and Cash Flow are included in the “Primary Financial Statements” section of the IFRS-CI Taxonomy. This applies whether or not the disclosures are made on the “Face” of the financial statements or in the footnotes to those statements. For example, details of inventories, such as “Raw Materials” or “Inventories” may be included on the Balance Sheet or in an Inventory note to the financial statements.

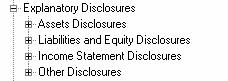

The “Explanatory Disclosures” elements in this IFRS-CI Taxonomy are designed for the reporting of disclosures that enhance the meaning of financial statement. The major elements of the Explanatory Disclosures are shown in Figure 16:

Figure 16: Enhanced Disclosures

Assets and Liability and Equity Disclosures

For each element in the Balance Sheet component of the Financial Statement Explanatory Disclosure (“Asset Disclosures” and “Liability and Equity Disclosures”), there is a relatively consistent structure that determines the closing balance of the asset or liability. This structure is illustrated in Figure 17. Whilst this general pattern holds, there are differences between classes of assets or liabilities that arise from the particular disclosure requirements of the IFRSs and/or from the essential nature of the item. For example, the disclosures for Investment Properties are necessarily somewhat different from those of Property, Plant and Equipment.

Figure 17: Structure of Changes in Assets or Liabilities

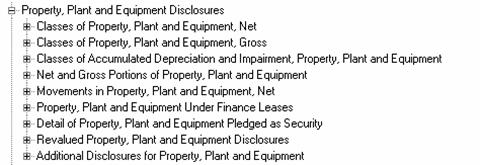

The makeup of Property, Plant and Equipment is shown in Figure 18:

Figure 18: Makeup of Property, Plant and Equipment

In addition, the nature of explanatory disclosures vary with the nature of assets or liabilities. Required disclosures on Deferred Tax are, for example, driven by the particular requirements of IAS 12.

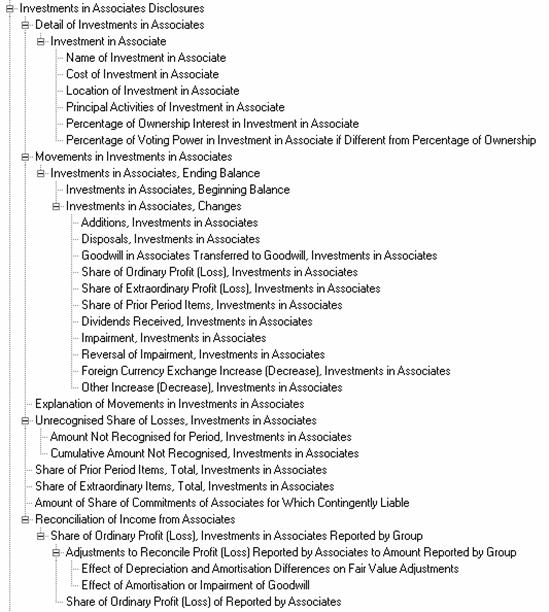

Certain classes of assets require additional disclosures beyond the details of movements. For example, a corporation may have an asset “Investments in Associates.” IAS 28 requires a number of additional disclosures that further explain these investments and particularly the changes in investments over the accounting period. These additional disclosures are covered by the elements shown in Figure 19:

Figure 19: Additional Disclosures on Investments in Associates

The “Investment in Associate” structure is a tuple that contains required disclosures on each significant associate, including name, cost of acquisition, location, principal activities, percentage of ownership interest and percentage of voting power in significant associate if different from percentage of ownership.” These elements will be repeated for each associate.

By contrast, the section “Movements in Investments in Associates” provides the closing balance of all investments in associates (“Investment in Associates, Ending Balance”). The opening balance of the associates (“Investment in Associates, Beginning Balance”) and the various changes (e.g. “Share of Ordinary Profit (Loss)”; “Dividends Received” and “Impairment”).

Income Statement Disclosures

The explanatory disclosures on the Income Statement component of the Taxonomy provide both descriptive, qualitative disclosures which explain the primary disclosures made in the Primary Financial Statements as well provide additional quantitative disclosures to supplement the disclosures made.

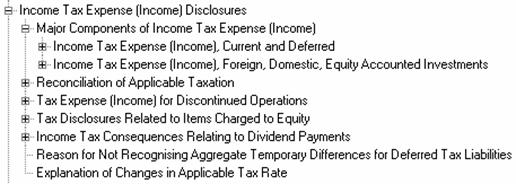

For example, the disclosures required by IAS 12 on income taxation are primarily additional quantitative disclosures to supplement the disclosure of income taxation, as shown in Figure 20:

Figure 20: Income Tax Expense (Income) Disclosures

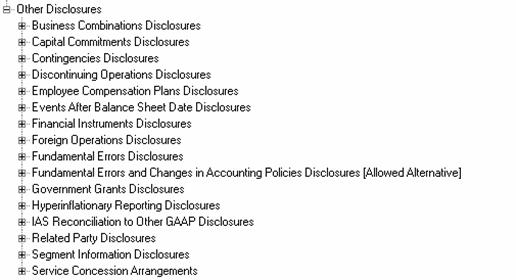

There are a variety of “Other Disclosures,” as shown in Figure 21:

Figure 21: Other Disclosures

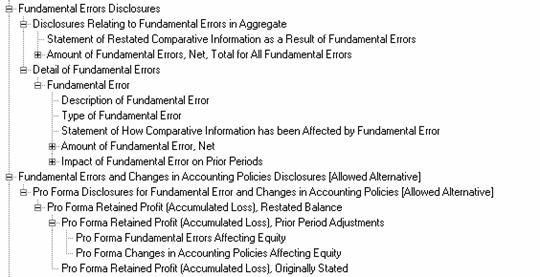

For example, IAS 8 requires a variety of disclosures on fundamental errors in the financial statements. The benchmark treatment of fundamental errors is shown in paragraphs 34 to 37 of IAS 8, reproduced below. The standard also allows an alternative treatment, as shown in Paragraphs 38-40:

* * *

Benchmark Treatment

34. The amount of the correction of a fundamental error that relates to prior periods should be reported by adjusting the opening balance of retained earnings. Comparative information should be restated, unless it is impracticable to do so.

35. The financial statements, including the comparative information for prior periods, are presented as if the fundamental error had been corrected in the period in which it was made. Therefore, the amount of the correction that relates to each period presented is included within the net profit or loss for that period. The amount of the correction relating to periods prior to those included in the comparative information in the financial statements is adjusted against the opening balance of retained earnings in the earliest period presented. Any other information reported with respect to prior periods, such as historical summaries of financial data, is also restated.

36. The restatement of comparative information does not necessarily give rise to the amendment of financial statements which have been approved by shareholders or registered or filed with regulatory authorities. However, national laws may require the amendment of such financial statements.

37. An enterprise should disclose the following:

(a) the nature of the fundamental error;

(b) the amount of the correction for the current period and for each prior period presented;

(c) the amount of the correction relating to periods prior to those included in the comparative information; and

(d) the fact that comparative information has been restated or that it is impracticable to do so.

Allowed Alternative Treatment

38. The amount of the correction of a fundamental error should be included in the determination of net profit or loss for the current period. Comparative information should be presented as reported in the financial statements of the prior period. Additional pro forma information, prepared in accordance with paragraph 34, should be presented unless it is impracticable to do so.

39. The correction of the fundamental error is included in the determination of the net profit or loss for the current period. However, additional information is presented, often as separate columns, to show the net profit or loss of the current period and any prior periods presented as if the fundamental error had been corrected in the period when it was made. It may be necessary to apply this accounting treatment in countries where the financial statements are required to include comparative information which agrees with the financial statements presented in prior periods.

40. An enterprise should disclose the following:

(a) the nature of the fundamental error;

(b) the amount of the correction recognised in net profit or loss for the current period; and

(c) the amount of the correction included in each period for which pro forma information is presented and the amount of the correction relating to periods prior to those included in the pro forma information. If it is impracticable to present pro forma information, this fact should be disclosed.

* * *

These disclosure items are reflected in the Taxonomy by the elements shown in Figure 22:

Figure 22: Fundamental Errors Disclosures

Important note: Where appropriate, disclosures in this section of the EDAP Taxonomy are linked to the PFS Taxonomy by “same-as” links.

3.9. Type Enumeration Elements

A Taxonomy section provides for type enumerations. Type enumerations are used to consistently identify (across entities expressing financial information using XBRL) in order to achieve comparability. For example, the IFRS-CI Taxonomy provides elements to disclose related party transactions. There are many types of related party transactions such as purchases or sales of goods, purchases or sales of property and other assets, etc. These types of related party transactions are listed, or enumerated, in the type enumerations section. The transactions with related parties section requests an element “Type of Related Party Transaction”. An element from the type enumerations section MUST be used, or the financial statement preparer MAY in their extension Taxonomy provide a type which would be used as a value for the “Type of Related Party Transaction” element within an instance document.

3.10. Equivalent facts (same-as, essence-alias)

These exceptions require the use of “same-as” definition links. The “same-as” or “essence-alias” concept is part of XBRL Specification Version 2.0a, and its interpretation is as follows: there will be an error if an instance document having two elements linked by a “same-as” definition relationship and which have the same numeric context have different content values.

Concept equivalency is discussed in section 5.3.5.7 of the XBRL Specification.

In the IFRS-CI Taxonomy, the following concept equivalencies exist:

|

Concept Equivalencies |

|

|

|

· Both “Profit (Loss) from Operations [by function]” and “Profit (Loss) from Operations [by nature]” are equivalent to “Profit (Loss) from Operations [by function or by nature]” |

|

· Both “Cash Flows from (Used in) Operations [Direct Method]” and “Cash Flows from (Used in) Operations [Indirect Method]” are equivalent to “Net Cash Flows from (Used in) Operating Activities [Direct or Indirect Method]” |

|

· “Equity, Total, Ending Balance” in the Statement of Changes in Equity is equivalent to “Equity Plus Minority Interest” in the Balance Sheet. |

Important Note: Concept equivalency is different from the use of multiple links to or from a single element.

3.11. Calculation Links

Financial statements are rich with relationships between the components of the financial statements. These relationships are expressed in XBRL using links. Currently, the IFRS-CI Taxonomy expresses a minimum amount of such relationships.

For example, by examining the Statement of Changes in Equity, one finds that calculation links are provided for the changes in each equity components. However, calculation links are not provided to express for example, that “Other Movements in Equity” for the change in each component of equity adds up to the element “Other Movements in Equity” for “Equity, Total”.

Note that there are 3 different calculation representation formats for the IFRS-CI balance sheet. These are:

· Order of Liquidity Format

· Current Non-current Format

· Net Assets Format

As resources to develop the Taxonomy further are made available and as tools are released to view and test these links, additional calculation links may be added to the IFRS-CI Taxonomy.

3.12. Presentation

The IFRS-CI Taxonomy does not endorse one presentation model for financial information over another any more, or any less, than IFRS endorses a single presentation model. The key information in the IFRS-CI Taxonomy is the expression of the elements used in financial reporting under IFRS and the relationships between those elements.

However, in order to physically present the Taxonomy in a 2-dimensional printed form or in a computer application, one presentation format must to be selected. The presentation format used mirrors the calculation links created to show relationships between the elements and further organised using a model which is common to accountants who prepare financial information and analysts who consume financial information.

For example, IFRS and common practice encourages the use of a classified balance sheet presented in liquidity order. Therefore, the IFRS-CI presents a classified balance sheet. In addition, the notes to the financial statements are organised in the same order as the balance sheet in order to provide an intuitive method to navigate the IFRS-CI Taxonomy; not to endorse one presentation model over another.

3.13. Definition Links

Definition links express “general-special”, “whole-part”, and “essence-alias” type relationships between taxonomy elements.

For example, “general-special” links are provided to indicate the accounting policies within the IFRS-CI Taxonomy. “Whole-part” relations are used to indicate which elements are contained within each accounting policy disclosure.

As resources to develop the Taxonomy further are made available and as tools are released to test these links, additional definition links may be added to the IFRS-CI Taxonomy.

3.14. Namespaces

Namespaces are an important XML concept. XBRL, using XML Schema 1.0, uses XML namespaces extensively in its schemas and instance documents. The purpose of a namespace, in the context of XBRL, is to identify the Taxonomy to which any particular XML element belongs. Namespaces allow software to resolve any ambiguity that may arise as a result of elements from different taxonomies sharing the same element name.

For example, the IFRS-CI Taxonomy uses the element name “CashCashEquivalents” to represent “Cash and Cash Equivalents”. If a different XBRL Taxonomy from, say, the United Kingdom also uses “CashCashEquivalents”, there must be a “differentiation” mechanism. This is accomplished by giving each Taxonomy a unique namespace. A namespace is a URI (Uniform Resource Identifier) such as http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15 (which is the namespace of this release of the IFRS-CI Taxonomy).

A namespace is not a URL (Uniform Resource Locator). It is a globally unique identifier. Within any XML document, it is not necessary to repeat lengthy identifiers with every Taxonomy element. Instead, XML allows one to define an abbreviation for each namespace used. Using “qualified” namespaces in this way, instance documents and taxonomies can define an alias such as ifrs-ci for the IFRS-CI Taxonomy, and uk for the UK Taxonomy. Thus the IFRS-CI element would be referred to as ifrs-ci:CashCashEquivalents and the UK element as uk:CashCashEquivalents – the namespace alias adds a context-establishing prefix to every XML element.

Note that these particular prefixes reflect a usage convention only within the IFRS-CI Taxonomy as an aid to communication between humans. Software applications must not depend on these particular prefixes being used; they should process namespace identifiers and namespace prefixes as specified by the XML specifications.

Important Note: XBRL instance document element names for financial concepts must be qualified names containing a namespace prefix and an element name, for example: ifrs-ci:CashCashEquivalents.

3.15. Entering Numeric Values into Instance Documents

Figure 13 describes how weights have been incorporated into the IFRS-CI Taxonomy and how corresponding values will be entered into an instance document.

Figure 23: Numeric Value Conventions

|

Balance |

Normally appears in instance document as |

|

|

Asset |

Debit |

Positive (Credit would be negative) |

|

Liability & Equity |

Credit |

Positive (Debit would be negative) |

|

Revenue |

Credit |

Positive (Debit would be negative) |

|

Expense |

Debit |

Positive (Credit would be negative) |

|

|

|

|

|

Other Income (Expenses) |

Credit |

Positive (Debit would be negative) |

|

|

|

|

|

Cash Inflows |

|

Positive |

|

Cash Outflows |

|

Positive |

|

|

|

|

|

Number of Employees |

|

Positive |

3.16. Segmentation

XBRL instance documents distinguish facts that relate to different segments of an entity by using the XBRL nonNumericContext and numericContext elements. For example, revenues for an entire entity, and its revenues segmented by geographical regions, e.g., Americas, Asia-Pacific, and EMEA, are each represented by using a different numericContext.

Important note: Instance documents using the IFRS-CI Taxonomy must use the entity context or the entity context segment mechanism to distinguish disclosures related to discontinuing operations where financial statement preparers have chosen to adopt the columnar approach of segregating continuing, discontinuing operations for a full primary financial statement (e.g. Cash Flows Statement ) illustrated in the Appendix to IAS 35. [Note that it is not possible to total activities across segments using the existing 2.0a specification]

Sample Company Sample Instance Document

3.17. Introduction

An example instance document that accords with the IFRS-CI Taxonomy, Sample Company, at http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/SampleCompany-2003-07-15.xml (XBRL/XML) and a Acrobat version of the accounts is at http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/SampleCompany-2003-07-15.pdf (PDF).

Sample Company sample instance document provides an example of how instance documents might apply the IFRS-CI Taxonomy.

3.18. Balance Sheet Example

Figure 24 shows the Consolidate Balance Sheet for Sample Company for the Year Ended 31 December 2002 with comparative information for 31 December 2001:

Figure 24: Balance Sheet of Sample Company

The instance document uses five contexts to represent information in the four statements. Three contexts represent instants in time: Current_AsOf for the 31 December 2002, Prior_AsOf for the 31 December 2001 and PriorPrior_AsOf for the 31 December 2000. The last item is required for the Statement of Changes in Equity There are two contexts for periods: Current_ForPeriod for the year ended 31 December 2002 and Prior_ForPeriod for the year ended 31 December 2001.

Taking Minority Interest as an example, the Balance Sheet shows €91,000 as at 31 December 2002 and €90,400 as at 31 December 2001. These facts are represented in the instance document as:

<ifrs-ci:MinorityInterestsNetAssets numericContext="Current_AsOf">91000</ ifrs-ci:MinorityInterestsNetAssets>

<ifrs-ci:MinorityInterestsNetAssets numericContext="Prior_AsOf">90400</ ifrs-ci:MinorityInterestsNetAssets>

The example above shows a namespace declaration ifrs-ci. When one follows the links within the instance document you will find:

xmlns:ifrs-ci="http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15"

The namespace declaration links the instance document back to the IFRS-CI Taxonomy.

The fact for Minority Interest for the Year Ended 31 December 2002 in the instance document also refer to the following Numeric Context: numericContext="Current_AsOf".

When one follows the links within the instance document one will find:

<numericContext id="Current_AsOf" precision="18" cwa="true">

<entity>

<identifier scheme="http://www.sampleCompany.com">Sample Company</identifier>

</entity>

<period>

<instant>2002-12-31</instant>

</period>

<unit>

<measure>iso4217:EUR</measure>

</unit>

One can see that this provides information on the entity, in this case Sample Company; the period, in this case the instant in time of 31 December 2002 and the currency, in this case Euros, according to the ISO 4217 enumerated list of currencies.

4. Reviewing this Taxonomy

4.1. Introduction

This section is designed to provide guidance in reviewing this Taxonomy and will be removed from the final version of this documentation. This section will assist the user of this documentation and of the Taxonomy to provide feedback to the IASCF and to XBRL International concerning the Taxonomy. There are three levels of review:

- Global Review: A high level review of Taxonomy completeness.

- Detailed Review: A detailed review of accounting disclosures.

- Preliminary XBRL Review: A review of appropriate treatment of disclosures within the context of the XBRL specification.

- Detailed XBRL Review: A review of appropriate treatment of disclosures within the context of the Financial Reporting Taxonomy Architecture (FRTA) Checklist of “best practice” Taxonomy building.

4.2. Global Review

This is a high level review, undertaken with the objective of ensuring the Taxonomy has not omitted any key sections. This contrasts with the Detailed Review, which is concerned with a line-by line analysis.

If a crucial part of the Taxonomy is missing, such as a specific Disclosure Note, this should be picked up in the Global Review. Some knowledge of IFRS and Financial Reporting is required to undertake this review.

The review is intended to identify missing sections of the Taxonomy rather than any missing element within a section. An example of a question that could be asked in the Global Review might be “are there elements that capture operating leases?” rather than validating each of the individual Lease Standard disclosures.

Other issues include:

Structure – nesting and completeness

Are the elements grouped in a sensible manner? To illustrate, this review would ask whether the elements that are nested under, for example, Finance Costs are appropriate. To answer this question requires a determination as to whether Finance Costs should reflect net or gross finance costs and an assessment as to whether the list of sub-elements appears complete.

Do the elements seem to roll up properly?

For example, net elements should have the ending balance as the parent element, with its component parts and gross amount expressed as its children elements.

Consistency

Are elements grouped or aggregated in a consistent manner? There may be cases where some parent elements appear to have a disproportionate number of children, and therefore provide detail that is more appropriately included elsewhere in the IFRS-CI Taxonomy.

4.3. Detailed Review

The objective of the Detailed Review is to ensure the Taxonomy correctly captures IFRS. It has two components, the first driven from IFRS and the second driven from XBRL.

IFRS Review

This review has a Financial Reporting focus, and involves validating the elements and disclosures in the Taxonomy on a line-by-line basis against IFRS.

Element accuracy is checked by reviewing the Taxonomy against:

- IFRS standards and reference materials;

- IFRS disclosure checklists;

- Model financial statements; and

- Actual financial statements

IFRS to XBRL

Reviewers should be able to identify an element in the Taxonomy for every item required to be disclosed under IFRS. This requires a 100% mapping from IFRS to the Taxonomy. This includes checking all the appropriate IFRS references.

There are many generic requirements to disclose a “component” for which there may be several classes. Examples include classes of shares, PPE (Property, Plant & Equipment) and expenses. The Taxonomy should only capture the most common classes observed in practice, to limit the need to build supplementary enterprise-specific taxonomies. In a similar manner, a standard may require the discourse of all “movements” in a particular item, such as capital.

This review should ensure that the element list is sufficiently complete in relation to all of these matters.

XBRL to IFRS

Not all elements in the Taxonomy will map directly to a IFRS disclosure requirement. Such elements exist in the Taxonomy because it is either 1) common practice for enterprises to disclose the fact or 2) the fact is a sub-total that helps derive the structural completeness of the Taxonomy.

4.4. Preliminary XBRL Review

This review has an XBRL focus, and involves verifying some of the attributes of the elements. The principal attributes to be verified are weights, labels and data-type.

Weights

Is the weight correct, so that the children correctly roll-up to the parent?

Labels

Label names should be consistent. For example, the net carrying amount of an asset might be labeled as “Description, Net”, such as “Goodwill, Net”. There should therefore be no cases of “Net Description” or any other variations. All abbreviations should also be consistent.

Data types

Is the element data type correct? For example, is a disclosure of textual information properly providing for a “string” data type, and numbers which have a currency associated with them providing for a “monetary” data type.

4.5. Detailed XBRL Review

This review has an XBRL focus, and involves reviewing the Taxonomy against a detailed checklist of financial reporting Taxonomy best practice requirements prescribed by the Domain Working Group.

5. Updates and Changes

5.1. Change Log

None at this time.

5.2. Updates to this Taxonomy

This Taxonomy will be updated with revisions for errors and new features within the following guidelines:

· Since financial statements created using a Taxonomy must be available indefinitely, the Taxonomy must be available indefinitely. All updates will take the form of new versions of the Taxonomy with a different date. For example, the Taxonomy http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2003-07-15/ifrs-ci-2003-07-15.xsd will never change. New versions will be issued under a different name, such as “http://www.xbrl.org/taxonomy/int/fr/ifrs/ci/2004-12-15/ifrs-ci-2004-12-15.xsd”. This will ensure that any Taxonomy created will be available indefinitely.

- It is anticipated that this Taxonomy will be updated as required to incorporate changes in International Accounting Standards, common practices, and business reporting norms.

5.3. Errors and Clarifications

The following information relating to this Taxonomy will be accumulated:

- Errors that are brought to the attention of the preparers of this specification;

- Workarounds where appropriate and available;

- Clarification of items which come to the attention of the editors via comments and feedback.

If you wish to report an error or require a clarification, please provide feedback as indicated in the “Comments and Feedback” section of this document.

5.4. Comments and Feedback

Comments and feedback are welcome, particularly ideas to improve this Taxonomy. If you have a comment or feedback or wish to report an error, post comments to:

xbrlfeedback@iasb.org.uk (mailto:xbrlfeedback@iasb.org.uk)

6. Acknowledgements

A tremendous effort has gone into creating this piece of intellectual property that is being licensed royalty-free worldwide by the IASC Foundation and XBRL International for use and benefit of all. The IASC Foundation and members of XBRL International believe that this cooperative effort will benefit all participants in the financial information supply chain.

The IASC Foundation and XBRL International would like to acknowledge the contributions of the following individuals for their work in the creation of this Taxonomy, and to their organisations that provided funds and time for their participation in this effort:

Name |

Organisation |

Accounting Jurisdiction |

|

Alastair Boult |

Audit New Zealand |

New Zealand |

|

Roger Debreceny |

Nanyang Technological University |

Singapore |

|

Kersten Droste |

PricewaterhouseCoopers |

Germany |

|

Thomas Egan |

Deloitte and Touche |

Singapore |

|

Dave Garbutt |

FRS |

South Africa |

|

Preetisura Gupta |

PricewaterhouseCoopers |

Singapore |

|

David Hardidige |

Ernst and Young |

Australia |

|

David Huxtable |

KPMG |

Australia |

|

Walter Hamscher |

Standard Advantage |

USA |

|

Charles Hoffman |

UBMatrix |

USA |

|

Josef Macdonald |

Ernst and Young |

New Zealand |

|

Gillian Ong |

Nanyang Technological University |

Singapore |

|

Ong Suat Ling |

Andersen |

Singapore |

|

Paul Phenix |

Australian Stock Exchange |

Australia |

|

Kurt Ramin |

IASC Foundation |

IFRS |

|

Jim Richards |

Murdoch University |

Australia |

|

David Prather |

IASC Foundation |

IFRS |

|

Trevor Pyman |

XBRL Australia |

Australia |

|

Julie Santoro |

KPMG |

Russia |

|

Mark Schnitzer |

Morgan Stanley |

USA |

|

David Scott-Stokes |

UBMatrix |

Australia |

|

Geoff Shuetrim |

KPMG |

Australia |

|

Stephen Taylor |

Deloitte and Touche |

Hong Kong |

|

Bruno Tesniere |

PricewaterhouseCoopers |

France |

|

Alan Teixeira |

Institute of Chartered Accountants |

New Zealand |

|

Jan Wentzel |

PricewaterhouseCoopers |

South Africa |

|

Charles Yeo |

Deloitte and Touche |

Singapore |

7. XBRL International Members

A current list of corporate members of XBRL International can be found at the www.xbrl.org web site.

8. References (non-normative)

|

Walter Hamscher et al. |

|

|

|

Extensible Business Reporting Language (XBRL) 2.0a Specification |

|

|

Contact walter@hamscher.com for the most current version. |

|

|

(http://www.xbrl.org/resourcecenter/specifications.asp?sid=22) |

|

|

|

|

Robert Blake, Walter Hamscher and David Prather |

|

|

|

Taxonomy Element Naming Best Practice Version 1.0 |

|

|

Working Draft of 2002-10-17. Contact mark.schnitzer@morganstanley.com for the most current version. |

|

|

|

|

[FRTA Checklist] |

Josef Macdonald and Charles Hoffman |

|

|

XBRL Domain Working Group: Quality Review Procedures for XBRL (Version 2.0a) Financial Reporting Taxonomy Approval. Contact josef.macdonald@nz.ey.com for the most current version. |

|

|

|

|

[Review] |

Josef Macdonald and Alan Teixeira |

|

|

Reviewing and XBRL GAAP Taxonomy |

|

|

Contact josef.macdonald@nz.ey.com for the most current version. |

9. Intellectual Property Status

This document and translations of it may be copied and furnished to others, and derivative works that comment on or otherwise explain it or assist in its implementation may be prepared, copied, published and distributed, in whole or in part, without restriction of any kind, provided that the above copyright notice and this paragraph are included on all such copies and derivative works. However, this document itself may not be modified in any way, such as by removing the copyright notice or references to XBRL International or XBRL organizations, except as required to translate it into languages other than English. Members of XBRL International agree to grant certain licenses under the XBRL International Intellectual Property Policy (www.xbrl.org/legal).

This document and the information contained herein is provided on an "AS IS" basis and XBRL INTERNATIONAL DISCLAIMS ALL WARRANTIES, EXPRESS OR IMPLIED, INCLUDING BUT NOT LIMITED TO ANY WARRANTY THAT THE USE OF THE INFORMATION HEREIN WILL NOT INFRINGE ANY RIGHTS OR ANY IMPLIED WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE.

The attention of users of this document is directed to the possibility that compliance with or adoption of XBRL International specifications may require use of an invention covered by patent rights. XBRL International shall not be responsible for identifying patents for which a license may be required by any XBRL International specification, or for conducting legal inquiries into the legal validity or scope of those patents that are brought to its attention. XBRL International specifications are prospective and advisory only. Prospective users are responsible for protecting themselves against liability for infringement of patents. XBRL International takes no position regarding the validity or scope of any intellectual property or other rights that might be claimed to pertain to the implementation or use of the technology described in this document or the extent to which any license under such rights might or might not be available; neither does it represent that it has made any effort to identify any such rights. Members of XBRL International agree to grant certain licenses under the XBRL International Intellectual Property Policy (www.xbrl.org/legal).

10. Document History

|

2003-07-10 |

Hoffman |

Updated URLs, images, references to taxonomy IDs, etc. Removed Novartis sample for this release as this sample is not being provided. |

|

2003-07-08 |

Macdonald |

Performed detailed review documentation. Added explanation of IFRS name change. Provided amendments as necessary. |

|

2003-06-23 |

Hoffman |

Merged the PFS and EDAP documentation into one document. Changed use of term ‘IAS’ to ‘IFRS’, as appropriate. Updated URLs. Changed all references to PFS and EDAP as required. |

11. Approval Process

This section will be removed from the final recommendation. IFRSWG = IFRS Working Group; ISC = International Steering Committee.

|

|

Stage (* - Current) |

Party responsible for decision |

Next step |

Revisions needed |

Target date for stage completion |

|

1* |

Internal WD |

IFRSWG |

Recommend for Stage 2 |

Stay in Stage 1 |

2003-07-01 |

|

2 |

Internal WD pending publication |

ISC |

Approve for Stage 3 |

Return to Stage 1 |

2002-07-05 |

|

3 |

Public WD under 45 day review |

WD Editors |

Minor revisions – to Stage 4 |

Major revisions, Restart Stage 1 |

2002-07-15 |

|

4 |

Draft Recommendation |

IFRSWG |

Recommend for Stage 5 |

Restart Stage 3 |

2002-09-01 |

|

5 |

Recommendation pending publication |

ISC |

Approve for Stage 6 |

Restart Stage 4 |

2002-10-01 |

|

6 |

Recommendation |

Done |

|

|

|