IFRS 18 and XBRL

This guest blog is by Shraddha Bagul, Lead Consultant at IRIS Business Services. She is co-chair of XBRL International’s Best Practices Board.

IFRS 18 Presentation and Disclosure in Financial Statements is a major change to financial reporting. Issued by the IASB in April 2024, it replaces IAS 1 and is effective for annual periods beginning on or after 1 January 2027, with earlier application permitted. It changes how information is presented and disclosed — most of all in the statement of profit or loss. Its introduction will affect every preparer that builds XBRL reports and every software vendor that maintains taxonomy tools.

IFRS 18 introduces three main changes for digital reporting: a required classification of income and expenses into five categories in the statement of profit or loss; the disclosure of management-defined performance measures (MPMs); and an updated IFRS Accounting Taxonomy. Anyone who prepares, reviews, or consumes digital financial reports should begin preparing now.

This blog is written for three audiences involved in the IFRS 18 digital reporting transition: XBRL report preparers; software vendors updating taxonomy tools and validation engines before the 2027 deadline; and regulators and data consumers that collect IFRS reports. It is a practical guide for those who build, validate, and consume XBRL reports, rather than for those focused on accounting policy or the conceptual framework.

What IFRS 18 Changes

IFRS 18 requires entities that apply IFRS to classify income and expenses in the statement of profit or loss into five defined categories. This should make income statements more consistent and comparable between companies. In effect, it is a move from more flexible presentation to a more structured, defined approach.

| 5 MANDATORY CATEGORIES

Operating, Investing, Financing, Income Taxes and Discontinued Operations |

MANAGEMENT-DEFINED PERFORMANCE MEASURES

New Disclosure and Audit Requirement |

| 2027- MANDATORY EFFECTIVE DATE

Annual periods beginning on or after 1 January 2027, with retrospective application and comparative statement |

TAXONOMY CONCEPTS ADDED

IFRS Taxonomy 2025 introduced hundreds of new elements to support IFRS 18 categorisation and MPM disclosures |

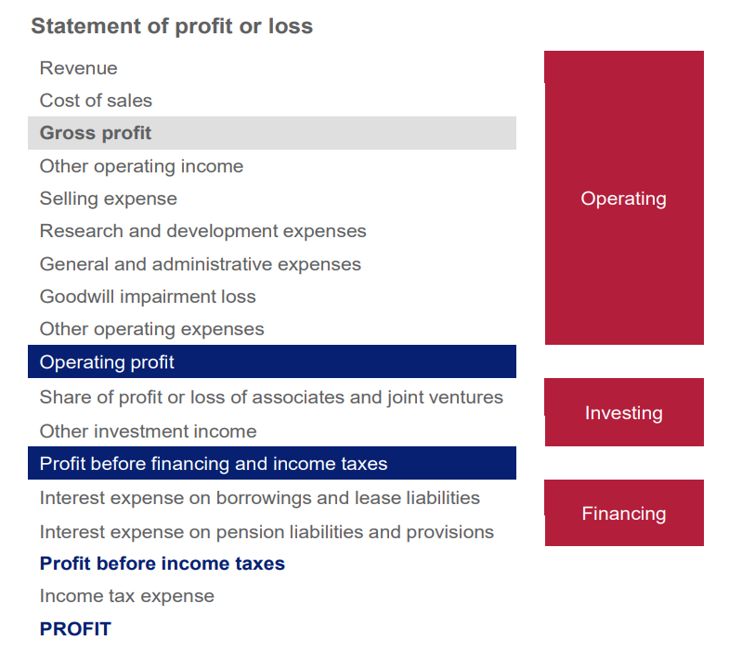

The most significant change in IFRS 18 is the structured statement of profit or loss built on the five categories. Previously, companies had flexibility in how they determined “operating profit,” and some presented related items in the notes or elsewhere. This reduced consistency and comparability. IFRS 18 now requires an “operating profit” subtotal — and a “profit before financing and income taxes” subtotal — which should improve comparability between companies.

The example above shows how the statement of profit or loss is mapped to the five IFRS 18 categorises. (Source)

Why Issuers Must Act Now

Before starting the tagging process, issuers should have the right systems, policies, procedures, and internal controls in place ahead of the 2027 deadline.

- Systems: ERP and reporting platforms must be able to capture income and expense data under both the IAS 1 and IFRS 18 classifications at the same time. Depending on the existing infrastructure, this may require restructuring the chart of accounts.

- Policies and procedures: Internal accounting policies must be updated to define how each line item is classified into the five IFRS 18 categories.

- Internal control: Transition adjustments should follow the same internal control checks as primary financial data. The audit committee should review the MPM disclosures in the financial statements, because MPMs are now within the audited financial statements and subject to external audit.

- XBRL/iXBRL tagging: During the transition, preparers must ensure their filings work with both the IAS 1 and IFRS 18 entry points, because comparative-period disclosures require dual tagging.

Impact on Preparers

For companies that prepare IFRS financial statements, IFRS 18 will require a certain amount of effort. Companies must review, and possibly redesign, their chart of accounts so that income and expenses are classified correctly into the five categories. Finance teams and financial controllers that produce XBRL/iXBRL reports for regulators (for example, ESMA or the SEC) will need to revisit how certain disclosures are tagged. IFRS 18 does not only add new line items; it also changes the digital tagging structure.

1.Remapping the statement of profit or loss.

Every income and expense concept in the statement of profit or loss must be mapped to one of the five IFRS 18 categories. Preparers who previously tagged line items using IAS 1 taxonomy concepts will need to check whether those concepts have been deprecated or revised in the IFRS Accounting Taxonomy 2025.

a) Map existing taxonomy concepts to the IFRS Accounting Taxonomy 2025.

Preparers should review the concepts that have been relabelled, added, or deprecated in the IFRS Accounting Taxonomy 2025.

The table below compares selected IAS 1 and IFRS 18 concepts.

| Financial Concept | IAS 1 Concept | IFRS 18 Concept | Status |

| Revenue | ifrs-full:Revenue | ifrs-full:Revenue | No change |

| Operating profit | ifrs-full:ProfitLossFromOperatingActivities | ifrs-full:OperatingProfitLoss | Change |

| Share of JV/Associate profit | ifrs-full:ShareOfProfitLossOfAssociatesAndJointVenturesAccountedForUsingEquityMethod | The element remains the same, but it is classified in the ‘Investing’ category.

The label is explicitly appended with the word ‘investing’. |

Category defined, Label change |

| Finance costs | ifrs-full:FinanceCosts | ifrs-full:InterestExpenseFinancing

Classified in the financing category for entities that do not have financing as a main business activity |

Element Change |

| Management subtotals (MPMs) | Entity-specific extension | Entity-specific extensions reconciled to the most directly comparable subtotal or total specified by IFRS. | New requirement |

Illustrative – Mapping of IAS 1 vs IFRS 18 Taxonomy Concepts

For more information, refer IFRS 18 Taxonomy webcast series

b) Identify deprecated or revised taxonomy concepts.

For example, a preparer may have used ifrs-full:ProfitLossFromOperatingActivities to tag operating profit in an annual iXBRL filing. This concept is deprecated under IFRS Taxonomy 2025 and replaced by ifrs-full:OperatingProfitLossOperating.

c) New validation check for the reconciliation of MPMs.

The IFRS Accounting Taxonomy 2025 includes an XBRL formula rule (a validation check) for reconciling MPMs with the related IFRS-defined subtotals. Preparers are encouraged to use this formula in their XBRL/iXBRL reporting. The formula checks that the management-defined performance measure equals the relevant IFRS total or subtotal, adjusted for the specified reconciling items.

d) Reclassify income and expenses across the operating, investing, and financing categories.

Under the IAS 1 taxonomy, finance costs were commonly tagged with ifrs-full:FinanceCosts. Under IFRS 18, such items must be classified by category (for example, operating versus financing) and tagged with the corresponding concepts.

2. Tagging management-defined performance measures (MPMs).

MPMs are a significant change under IFRS 18. Companies must bring certain non-GAAP measures (such as Adjusted EBITDA or Underlying Profit) into the audited financial statements. Each entity-specific subtotal must be reconciled to the most directly comparable subtotal or total specified by IFRS.

From a digital reporting perspective, this is challenging. Since MPMs are entity-specific, preparers cannot rely only on standard IFRS concepts. They must create an entity-specific (extension) element for each measure and anchor it to the closest IFRS Accounting Taxonomy concept. Equally:

- MPMs must be disclosed in a single note to the financial statements.

- Preparers must apply the dimensional structure defined for MPM disclosures to reconcile each MPM to its most directly comparable IFRS-defined subtotal.

- Management must explain why the measure provides useful information, how it is calculated, and any change in how it is calculated.

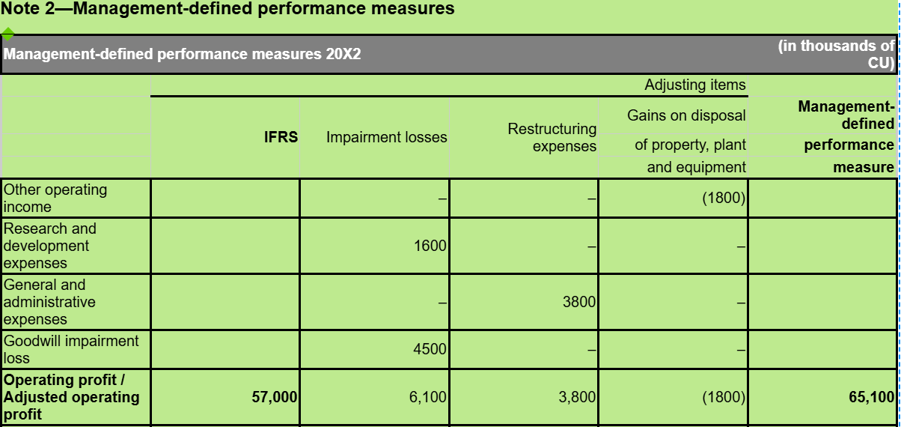

Illustrative MPM reconciliation example

The extract below, from the IFRS illustrative examples, shows how a company that discloses “Adjusted operating profit (loss)” as an MPM would reconcile it to the IFRS-defined subtotal “Operating profit (loss), operating”

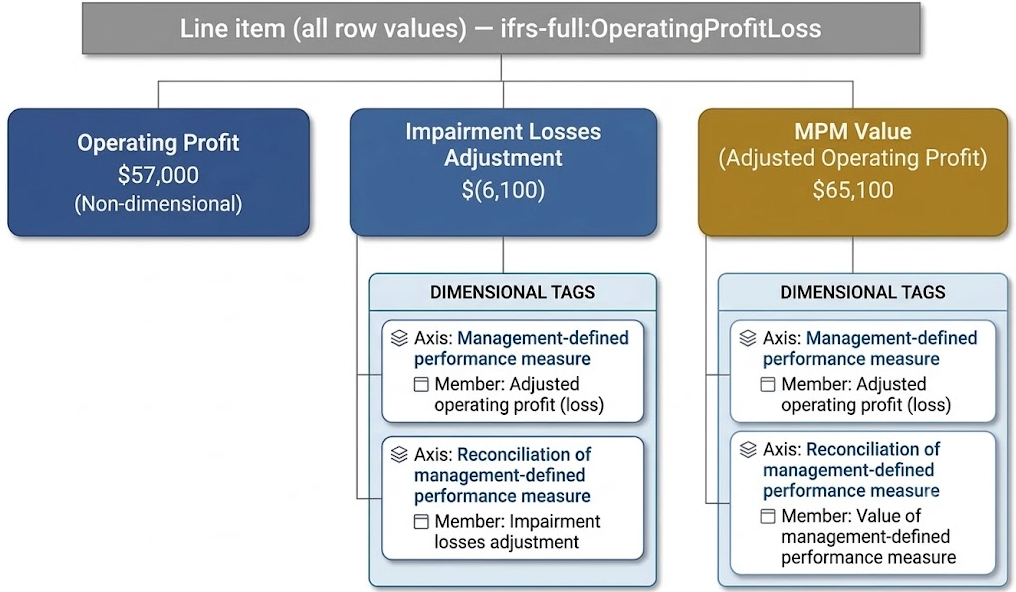

Now let’s understand how the XBRL tagging will be applied to the above MPM disclosure for Total Operating profit/Adjusted operating profit values using the dimensional structure defined in the taxonomy.

Only the impairment losses adjustment is expanded here for illustration; the same dimensional tagging logic applies to all other reconciling items.

- Operating profit (57,000) – This value will be tagged using the line item “ifrs-full: OperatingProfitLossOperating”. The same line item will apply to both the reconciliation items and the MPM value.

- Impairment Losses Adjustment: (6,100) – This value will be tagged using two extension members across two distinct IFRS taxonomy-defined axes:

- Management-Defined Performance Measures Axis: Tagged with the extension member Adjusted operating profit (loss) [member].

- Reconciliation of Management-Defined Performance Measure Axis: Tagged with the extension member Impairment losses adjustment [member] to identify it as a reconciling item.

- MPM value (65,100) – This value will be tagged using two members to represent the final performance measure:

- Management-Defined Performance Measures Axis: Tagged with the extension member Adjusted operating profit (loss) [member].

- Reconciliation of Management-Defined Performance Measure Axis: Tagged with the pre-defined base taxonomy member Value of management-defined performance measure [member].

3. Comparative Period Restatement

IFRS 18 requires comparative periods to be restated. Companies will need to reclassify their prior-period Statement of Profit or Loss line items to fit the new structure. For preparers, this likely leads to “dual tagging” during the transition.

4. Aggregation and Disaggregation Disclosures

IFRS 18 introduces a more structured, principle-based approach to aggregation and disaggregation. Entities must group items that share characteristics and separate items that are different, so the information is neither too summarised nor too detailed. For example, a company might present a single “Employee costs” line on the face of the statement of profit or loss, and disclose a further breakdown in the notes. Preparers should therefore treat the move to IFRS 18 not only as a reporting exercise, but as a chance to check whether the reported data are detailed enough to support the disclosures the standard now requires.

Impact on Software Vendors

Vendors of report preparation tools, XBRL validators, data aggregators, and taxonomy management platforms will need to update their systems in various ways and will need to be aware of a range of issues including:

- Taxonomy version update

Software vendors must integrate the IFRS Accounting Taxonomy 2025 updates into their platforms, including the entry points that support early adoption of IFRS 18. Product updates should be released well before the 2027 deadline to give clients enough time to prepare. Vendors should validate their software against the latest taxonomy and conformance suites to confirm that their tools produce compliant XBRL under both the IAS 1 and IFRS 18 entry points.

- Mapping disclosures and calculation logic

Every statement of profit or loss disclosure based on IAS 1 must be updated to meet IFRS 18. Vendors must also update the calculation logic for “operating profit.” Errors in this logic will likely cause a filing to fail validation, depending on the regulator’s rules. Overall, software vendors and service providers will need to:

- Restructure the statement of profit or loss disclosures to align with the five IFRS 18 categories:

- Update the calculation logic for the required subtotals, specifically for “operating profit” and “profit before financing and income taxes.”

- Implement the data required for MPMs and their reconciliations.

- Support both the IAS 1 and IFRS 18 entry points. Entities that early-adopt IFRS 18 must use the IFRS 18 entry point; entities still applying IAS 1 continue to use the IAS 1 entry point until they adopt IFRS 18.

- Validation rule updates

Vendors must update their XBRL validation engines to reflect the latest filing manuals from regulators such as the FCA and ESMA. The IFRS Accounting Taxonomy 2025 package includes a XBRL formula rule that provides a validation check for the reconciliation between MPMs and the related IFRS-defined subtotals. Although the rule is included in the taxonomy package, it is not imported through the taxonomy entry points. Preparers and vendors are encouraged to use this formula in their tagging and validation.

- Data consumers and API providers

Users of financial-data analytics platforms will benefit from the improved structure and comparability of IFRS 18 statements. These platforms will need to update their data models to handle the new categories and MPM disclosures. Historical time-series data should be carefully restated or flagged to avoid misleading comparisons between pre- and post-IFRS 18 figures.

Impact on Regulators

Regulators should benefit from IFRS 18, because the defined structure and consistent subtotals will make structured financial data more comparable across filers. The transition also creates responsibilities for regulators in how they prepare for, validate, and consume IFRS 18 data.

Impact on data collectors – Regulators and data collectors will need to update their systems to receive, process, and validate filings under both the IAS 1 and IFRS 18 entry points during the transition. Downstream agencies must ensure their data pipelines, storage models, and analytical tools can tell the two entry points apart.

Impact on filing rules and validation frameworks – IFRS 18 will require updates to existing XBRL filing rules across the major regulatory frameworks. Regulators must review and revise their filing manuals and validation rules to reflect the new IFRS Accounting Taxonomy 2025 statement of profit or loss and MPM disclosure requirements.

Conclusion: Preparing For the IFRS 18 Digital Reporting Transition

IFRS 18 is not a routine taxonomy upgrade. It is a significant change in how IFRS financial statements are presented, structured, and digitally tagged. By requiring defined categories in the statement of profit or loss and the disclosure of management-defined performance measures (MPMs), it is one of the more substantial changes to financial presentation in many years. Preparers should act now: run a gap analysis and plan for the “dual-tagging” of comparative periods well before the January 2027 deadline. If they have not done so already, XBRL software vendors should give priority to updating their taxonomy engines and validation rules to support the transition. Together, these changes give investors and regulators higher-quality digital information to support their decisions.