Enhancing Comparability with Anchoring

This is a post by XBRL International’s Entity Specific Disclosure Task Force (ESDTF).

Taxonomy authors expend considerable effort identifying common practice reporting (CPR) elements for inclusion in taxonomies such as the IFRS and US GAAP taxonomies. Filers frequently meet reporting requirements that are not explicitly defined in the accounting standards by creating extension elements. This use of extensions reduces data comparability, however, making it important to capture widely used concepts within taxonomies wherever possible. The process for identifying and grouping these extension elements as CPR elements has tended to be time consuming as there are often many extension elements across many filers with the same meaning, but no simple way to identify them as the same concept.

The first step is to identify all extension elements in a population of filers, which is a straightforward data pull of elements using a custom namespace. However, grouping these extensions by a common characteristic can be considerably more complicated. A variety of techniques have been used including matching label content and common standard relationships defined in the base taxonomy elements, but these methods remain time intensive. However, with the introduction of anchoring for European Securities and Market Authority (ESMA) reports, we now have an additional technique that promises to enhance this classification process where anchoring is required by a regulator.

Anchoring, as required by European Single Electronic Format (ESEF), links an extension element created by the preparer, to an appropriate element in the ESEF taxonomy that is either wider or narrower in accounting meaning or scope. Analysts, regulators and other users can use this information to better interpret and compare financial information collected through the use of extensions.

CPR element identification using the anchoring relationships

Under the European Securities and Market Authority (ESMA) ESEF rules, all extension elements are required to be anchored using the wider-narrower relationship (arcrole). This relationship can be used to help group CPR elements that have an implied common meaning by virtue of their common anchor point.

Analysis to identify extension elements suitable for adding to a base taxonomy as a CPR element, is made up of the following steps.

NOTE: Query filings to pull all extension elements including related arcroles.

1. Identify extension elements for all filings in scope using:

- Custom element namespace since all extensions are included in the filer’s schema.

- Other methods that may be available as a result of regulations or as provided in software tools, e.g., the ESMA requirement to list line-item extensions in the 999999 presentation group.

Figure 1 is an example list of extension elements identified across the sample reports.

The extension elements are listed as “QNames”: the combination of a short prefix and the element name. The ‘custom’ prefix is drawn from the namespaces of the extended taxonomies.

Figure 1: List of extended elements

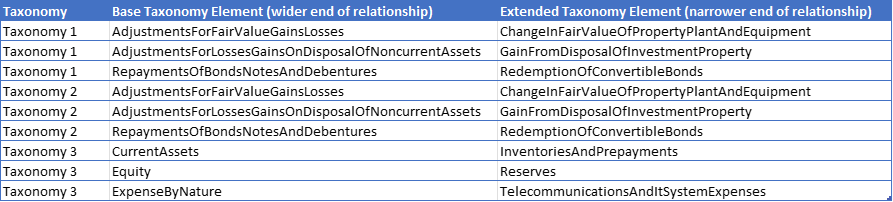

2. Group extension concepts using the wider-narrow relationship – applicable to both the wider and narrower aspects.

- The primary benefit derives from aggregating extensions by the wider base taxonomy element anchor.

- A secondary benefit derives from aggregating by the narrower base taxonomy element anchor.

The extended elements need to be logically grouped to understand their context and enable meaningful analysis. The wider-narrower relationship available for extension elements in the ESEF reports is helpful for such analysis.

Figure 2 is an example of wider-narrower relationships extracted from three extended taxonomies where the wider end of the relationship is anchored to the base taxonomy element.

Figure 2: Elements with Wider-Narrower relationships. Wider Element in the Base Taxonomy

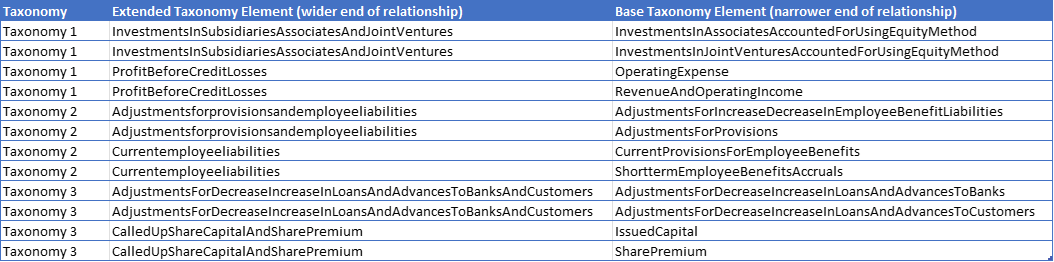

Similarly, the extended elements anchored where the narrower end of the relationship is anchored to the base taxonomy element are listed in Figure 3.

Figure 3: Elements with Wider-Narrower relationships. Wider Element in the Extended Taxonomy

3. Group extension structural elements (tables, axis, and domain members) using dimension syntax. While this step does not rely on the wider-narrower relationship, it is a part of the overall grouping of extensions process. Figure 4 is an example of a list of domain members extended. The dimension hierarchy is used to understand the dimension in which the extended members were defined

Figure 4: Extended domain members connected to dimension

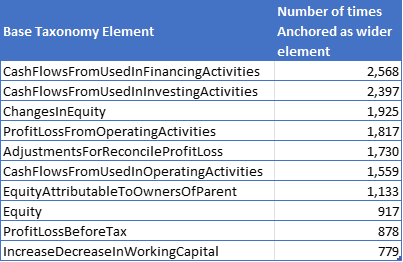

4. Summarise extension count by wider anchor and, to the extent possible by statement, i.e., ranking high to low (note that the top of the list will probably be dominated by cashflow related extensions. These can be a challenge to identify commonality as the common cashflow anchors are very general and the extensions here are often very different. Looking further down the list should show common threads.

- It is helpful to identify commonly used wider anchors for extensions. These are areas where issuers are often using a higher degree of granularity. This will assist with focus.

- Commonly used narrower anchors indicate scenarios where filers frequently aggregate or net base taxonomy elements. Including the narrower anchor points will assist with further grouping and ranking.

As illustrated here, this step identifies commonly used wider anchors for extensions. This is achieved by deriving the count of wider elements anchoring for extensions across the report from a list, as given in Figure 2. For a sample study of 3100 ESEF reports in 2021, Figure 5 lists the top 10 base taxonomy (IFRS) elements anchored as wider elements.

Figure 5: Top 10 IFRS elements anchored as wider elements

Similarly, a count of top base taxonomy elements that were anchored as narrower elements can be determined.

5. Break down extensions by nature:

- Extensions that do not require further action for including in the base taxonomy

- Extensions that are available in a subsequent base taxonomy release

- First group where element names match

- Second group that match semantically based on label and contextual analysis

- Extensions that should not have been created because there is an appropriate base taxonomy element available

- Extensions that conflict with the underlying accounting standards or other reporting requirements

- Extensions that are available in a subsequent base taxonomy release

Which leaves us with

- Extensions that are candidates for CPR elements

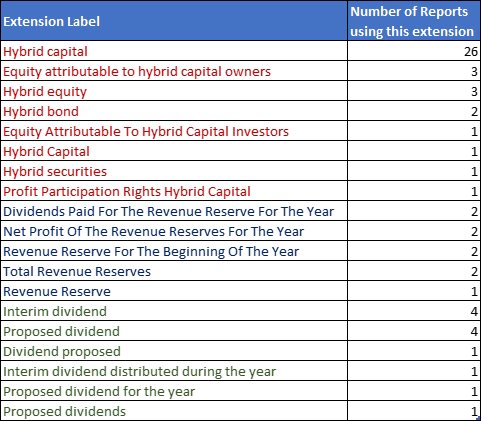

Having gained an understanding of base taxonomy elements that filers frequently aggregate or net, the next step is to investigate whether patterns exist in the extension elements. For example, let’s consider the base taxonomy element “Equity.” Figure 5 states there are over 900 extensions anchored to Equity. To understand these hundreds of extensions, they need to be further classified. One method here is to use the extension labels, categorising them in the same bucket based on text similarity.

Figure 6 is an extract of a few extension elements anchored to “Equity,” grouped based on the clustering output. Labels in the same colour belong to a group with similar text.

Figure 6: Clustering of extension elements anchored to ‘Equity’

“Hybrid capital” is a common pattern in extensions in the first group; this gives helpful insight into how multiple companies have extended similar concepts.

Using the wider-narrower relationship and grouping similar extension text helps better analyse CPR elements, offering improved insights over a laundry list of extension elements.

6. Apply the taxonomy author’s criteria for including CPR in the base taxonomy. Our separate guidance explains the criteria and how to include CPR in taxonomy.

In summary, leveraging anchoring to help group extension elements by this commonality should save time in identifying CPR elements for taxonomy inclusion. Check out this dashboard to explore extensions grouped by labels from the 2022 ESEF report, created using the steps outlined in this blog post.

Readers can contact the Entity Specific Disclosure Task Force at esd@xbrl.org