This document is a review draft. Readers are invited to submit comments to the Implementation Guidance Task Force.

Table of Contents

1 Abstract

The XBRL standard provides a number of different formats for digital reports. This guidance document explains different reporting scenarios and when to select Inline XBRL as the report format. This document is targeted at collectors and solution architects to help them identify the appropriate implementation choice.

2 XBRL report formats

The XBRL standard provides the following interoperable formats for representing digital reports to meet different business requirements:

- xBRL-XML: the conventional XML format defined by the XBRL v2.1 specification.

- Inline XBRL (iXBRL): a format for embedding XBRL tags within a human-readable, HTML document.

- xBRL-JSON: a simple, JSON-based format for XBRL data.

- xBRL-CSV: an efficient, CSV-based format, particularly well-suited for bulk data reporting.

All types of report provide tagged data in the form of a set of facts. Each fact provides a value for a concept defined in a taxonomy. For example, a report might provide the value $1m for the concept “Profit”. In addition, the fact includes some contextual information such as the period to which the fact applies and the units it is reported in.

Whereas an xBRL-XML, xBRL-JSON or xBRL-CSV report provides only the tagged data, an iXBRL report is a human-readable report with tagged data embedded in it. The tagged data in an iXBRL report can be extracted and converted into an XBRL report by an iXBRL processor. At a technical level, xBRL-XML, xBRL-JSON and xBRL-CSV reports can only be read with XBRL software. An iXBRL report is an HTML document that can be viewed directly in a web browser, as well as consumed using XBRL software.

3 Open and closed reporting

Business reporting requirements fall broadly into two categories, "open reporting" and "closed reporting". Closed reports are analogous to a paper form: the receiver of the report prescribes the information that must be reported as a set of boxes on the form, and the preparer files the data by filling in the boxes. The report may allow certain flexibility, such as repeating a row in a table as many times as needed, but there is no scope for the preparer providing information that is not covered by the form.

By contrast, in an open report, the preparer has control over both the information that is reported, and how it is presented. Open reports are most commonly encountered as company financial reports, where a company must adhere to accounting standards that prescribe rules or principles for what must be reported, but which do not define a reporting “form” or “template”. Such reports may require the preparer to disclose information that is specific to the reporting entity (an entity-specific disclosure).

It should be noted that the distinction between “open reporting” and “closed reporting” is a feature of the reporting requirements themselves, and does not depend on how those requirements are implemented in an XBRL report collection environment.

3.1 Presentation requirements

In almost all reporting environments, there is a need to be able to display the report in a human-readable format, but this is a very different process for a closed report compared to an open report.

In a closed reporting environment, the collector of the report will often prescribe a standard layout used to describe the data to be reported. The same layout is often also used to display reported data. Even where this is not done, because the data contained in a closed report is constrained, it is straightforward to take just the reported data and present it in whatever format is most useful to the consumer.

In an open reporting environment, the preparer typically has significant control over the layout and formatting of the report, and if a consumer receives only the data, it is impossible to reconstruct the human-readable version of the report that the preparer originally envisaged. Further, the report may contain entity-specific disclosures that can be very difficult to present meaningfully in a human-readable report if only the data is received. Therefore, open reporting environments typically have a requirement for preparers to provide a human-readable version of the report, as well as tagged, structured data.

3.2 Open and closed reporting: key characteristics

Table 1 summarises the characteristics of open and closed reporting.

|

Feature |

Open Reporting |

Closed Reporting |

|

Reporting Data |

Reported data is determined by the preparer, in accordance with rules or principles. This may include entity-specific disclosures. |

Data to be reported is prescribed by the collector. |

|

Flexibility in reporting |

Data reported will vary according to entity’s specific situation and may include judgements based on materiality. |

None. Data must be reported in accordance with the prescribed rules. |

|

Layout of report |

Preparer defined and flexible. |

Generally proposed by the collector. |

|

Report rendering requirement |

Preparer-defined report layout required for comprehensive understanding. |

Can be viewed using standardised report format. This is typically provided by the collector. |

4 XBRL formats for closed reporting environments

In closed reporting, the data set being reported is well-defined and there is no need for a preparer to provide their own presentation of the report. It is sufficient to collect just the data, and it can be visualised in whatever way the collector prefers, which typically takes the form of a standard template. As such, xBRL-XML, xBRL-JSON or xBRL-CSV, rather than iXBRL, is suitable as the report format.

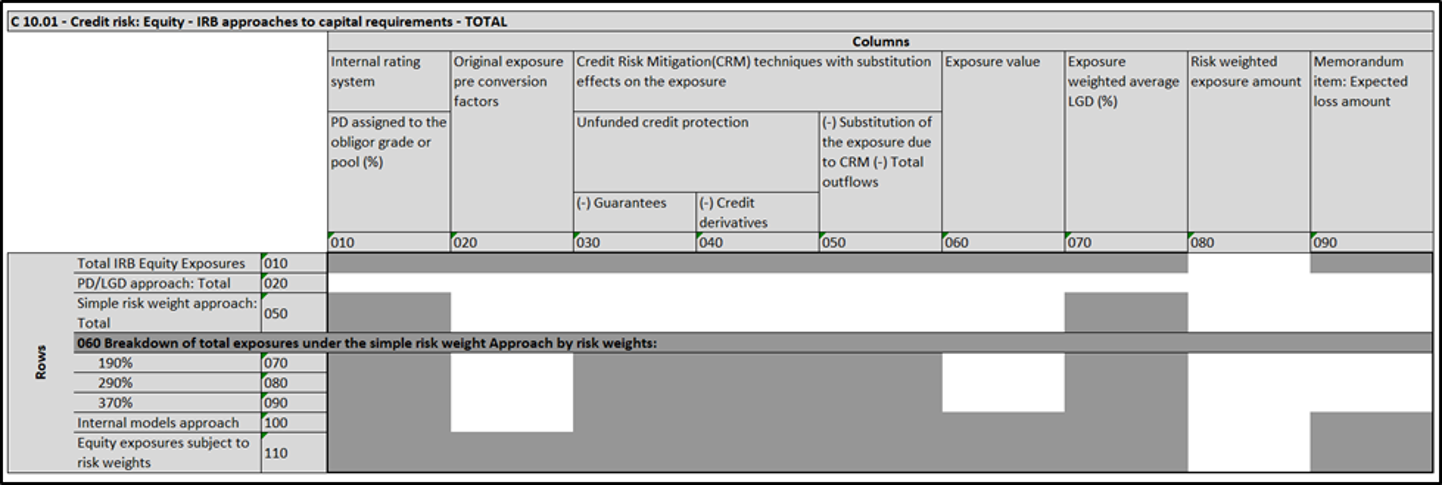

XBRL provides a standard way for taxonomy authors to define business-user friendly table structures, known as XBRL reporting templates (Table Linkbase). These table structures can be used by preparers to prepare or render data in XBRL reports. Figure 1 shows an extract from a business template created using the Table Linkbase. This example is taken from the European Banking Authority’s taxonomy for credit risk reporting.

Figure 1: XBRL reporting template

Figure 1: XBRL reporting templateThe Table Linkbase provides a powerful mechanism for defining reporting templates, supporting highly dimensional data, and dynamic tables where additional rows and columns can be added as required. To find out more about Table Linkbase read this separate piece of guidance which explains features of Table Linkbase.

xBRL-CSV allows data collectors to define metadata for a fixed CSV template enabling preparers to focus on creation of CSV data tables. Detailed information about the xBRL-CSV format can be found in the xBRL-CSV tutorial.

5 iXBRL for open reporting environments

Where structured data is collected in an open reporting environment, preparers generally create both a human-readable report, and structured (e.g. XBRL) data. The preparer-formatted human-readable report is typically created to publish on a website, for investor relations communications or for regulatory submission. The risk of inconsistencies and/or confusion between the two versions of the report cannot be ruled out.

iXBRL avoids the need for preparing two separate reports. Since iXBRL embeds tagged data in a human readable report, a single filing serves both the purposes of human and machine consumption and creates a direct link between the structured data and the presentation.

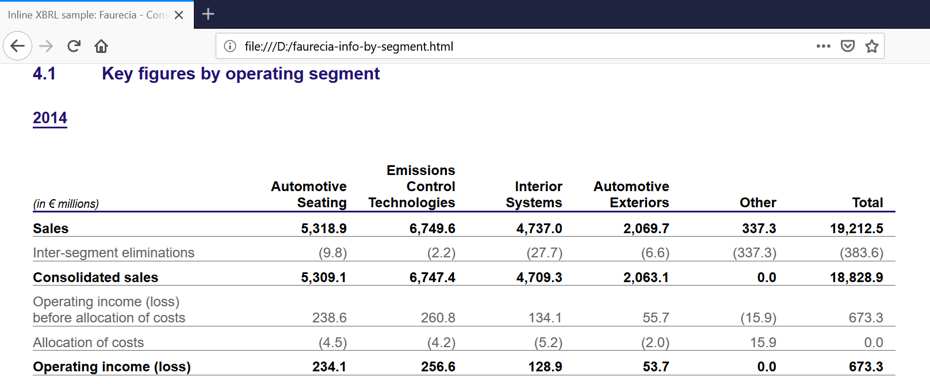

Figure 2 shows a sample iXBRL report as it appears when viewed in a normal web browser. As can be seen, no special software is required in order to view the human-readable version of the report.

Figure 2: iXBRL report viewed in a web browser

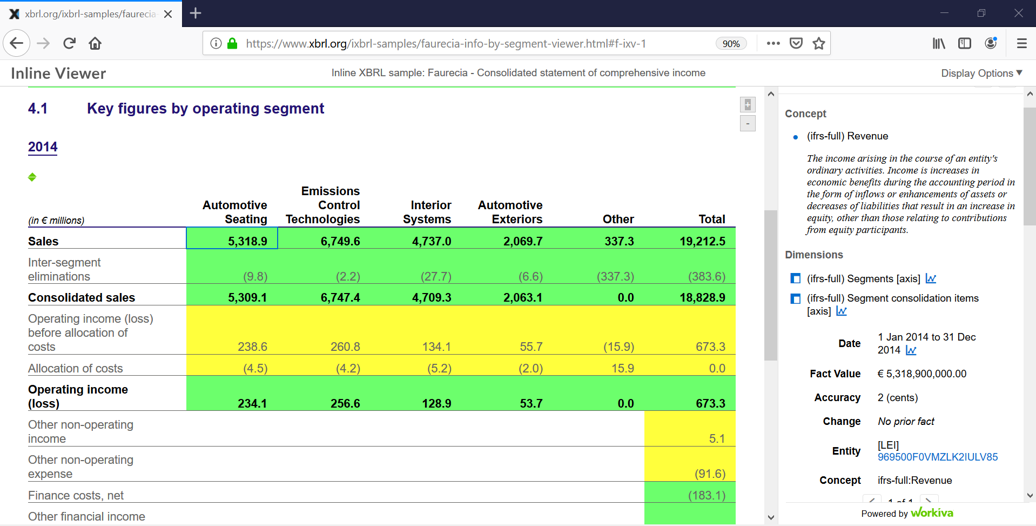

Figure 2: iXBRL report viewed in a web browserFigure 3 shows the same iXBRL document using iXBRL viewing software. The tagged items are highlighted, and can be clicked on to show details of how they have been tagged.

Figure 3: iXBRL report viewed in iXBRL software

Figure 3: iXBRL report viewed in iXBRL softwareiXBRL software can provide many features to make the report more interactive. For example, existing software products enable:

- Easy navigation between the different places the same fact is presented within the report.

- Searching for facts based on information in the taxonomy, such as references to accounting standards.

- Highlighting of any facts in the report that fail automated quality or consistency checks.

- Display of taxonomy concepts and taxonomy-defined dimensions in different languages (if multi-lingual labels are available).

6 iXBRL and entity-specific disclosures

As noted above, open reports will often include entity-specific disclosures. The requirement for entity-specific disclosures is often addressed using entity-specific extension taxonomies. Extension taxonomies can be used by all XBRL report formats, but iXBRL reports have the advantage of including a human-readable presentation of the extension data, which can otherwise be challenging for applications to render.

In some environments, the use of iXBRL can reduce the need for extensions in the first place. If the consumer of the reports is only intending to perform automated analysis on data tagged against the base taxonomy, then it may be sufficient for any entity-specific disclosures to be left untagged, and available only in human-readable form. By combining the human-readable report and tagged data into a single document, such partial tagging is viable, as all information is included in the human-readable form. The linking of the data that is tagged provides the ability to interactively navigate quickly from data that has been reported and analysed against the base taxonomy to viewing the data in context, alongside untagged facts in the human-readable view.

This approach is primarily applicable where the collector of the report is the only consumer of the data, and can say for certain what analysis will be performed on the data. This would typically be the case for a tax authority that does not publish the reports that it collects.

By contrast, where a collector publishes the reports that it receives, it is not possible to know how the data will be consumed and analysed by third parties, and the inclusion of entity-specific disclosures tagged against an extension taxonomy may be beneficial. An example of this would be securities regulator collecting company financial reports and publishing them for the benefit of investors and analysts.

7 Summary and recommendations

In general, iXBRL is the recommended solution for open reporting requirements. It enables a single document to provide both tagged data and a human-readable report, and allows preparers to retain fine-grained control over the presentation of their report. iXBRL’s approach of embedding tags into the human-readable report enables a greater degree of interactivity when viewing reports, and simplifies the task of ensuring that human-readable and machine-readable data is consistent. The use of iXBRL avoids the need for preparation of separate human readable and structured reports, and reduces the associated risk of inconsistency between the two.

In a closed reporting environment, xBRL-XML, xBRL-JSON, or xBRL-CSV reports are the recommended choice. In such environments, there is no need for preparers to provide their own presentation of the data. Human-readable reports can be generated from the reported data, using mechanisms such as XBRL reporting templates (Table Linkbase).

A detailed guide for selecting amongst xBRL-XML, xBRL-JSON, and xBRL-CSV is discussed in separate guidance.

Table 2 summarises the comparison between XBRL report formats.

|

Feature |

iXBRL |

xBRL-XML, xBRL-JSON, xBRL-CSV |

|

Primarily suitable for |

Open reporting |

Closed reporting |

|

Supports tagging of data |

Yes |

Yes |

| Data content |

Defined by the taxonomy, including any extension taxonomies (where applicable). |

|

|

Preparer has control over presentation of report |

Yes |

No (extension taxonomies may provide limited control over rendering, where permitted) |

|

Report can include untagged information, as well as tagged data |

Yes |

No |

|

Report can be viewed without XBRL software |

Yes, although XBRL-enabled software can provide a more interactive user interface |

No |

|

Submission of human readable report and tagged data |

One report serves both functions |

Not supported (must be submitted separately, if required) |

- iXBRL is the recommended solution for open reporting requirements, where the preparer has control over both the information that is reported, and how it is presented.

- xBRL-XML, xBRL-JSON or xBRL-CSV are the recommended solution for closed reporting requirements, where data to be reported is prescribed by the collector.

This document was produced by the Implementation Guidance Task Force.

Published on 2019-10-10.